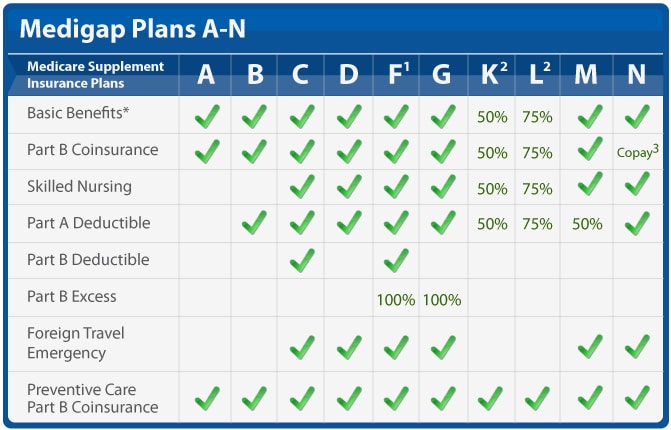

Plan GCategory:

Are you ready to dive into the intricate world of Medicare Supplements? If you’re exploring your options, you’ve probably come across Medicare Supplement Plan N and Plan G. While both plans offer comprehensive coverage, what are the differences between Medicare Plan N vs Plan G?

Supplement Plan N and Plan G. While both plans offer comprehensive coverage, what are the differences between Medicare Plan N vs Plan G?

In this essential guide, we’ll take a closer look at Medigap Plan N and Plan G to help you determine the right fit for your healthcare needs. From coverage details to cost considerations, we’ll cover all the essential aspects to make your decision-making process easier.

Whether you’re new to Medicare or considering switching from your current plan, this guide will provide valuable insights. By the end, you’ll clearly understand each plan’s benefits and potential drawbacks, empowering you to choose the best option for your unique circumstances.

So, grab a cup of coffee, sit back, and let’s explore the intricacies of Medicare Plan N vs Plan G. Aren’t you curious to find out which plan will provide the best coverage for you?

Overview of Medicare Plan N

Overview of Medicare Plan N

Medicare Plan N is a popular choice for individuals who want comprehensive coverage at a more affordable price. Plan N, like Plan G and the other plans, cover virtually everything. Medicare is the most comprehensive health insurance out there. The key difference of Plan N is the cost-sharing structure, which requires you to pay a small copayment or coinsurance for certain services.

Like all Medicare supplement plans, you’ll be free to choose your own healthcare providers with plan N, as the plan doesn’t require you to select a primary care physician or obtain referrals for specialist visits. All physicians and health facilities that accept Medicare will also accept the supplement. This flexibility can be especially beneficial if you prefer to have control over your healthcare decisions.

While Plan N covers a significant portion of your healthcare expenses, it does come with some out-of-pocket costs. For example, you’ll be responsible for paying the Part B deductible and any excess charges that exceed the Medicare-approved amount. However, these costs are usually minimal compared to the plan’s overall coverage.

Medicare Plan N offers a comprehensive range of coverage and benefits.

Here is what is covered:

1. Part A Hospital Coverage: Plan N covers hospital stays, including room and board, nursing care, and other related services.

2. Part B Medical Coverage includes coverage for doctor visits, outpatient services, and preventive care.

3. Emergency Care: Plan N covers emergency room visits and urgent care services.

4. Skilled Nursing Facility Care: If you require skilled nursing care, Plan N covers the costs of this type of facility.

5. Hospice Care: Medicare Plan N includes coverage for hospice care, ensuring that you receive the necessary support during end-of-life care.

In addition to these core benefits, Plan N offers coverage for certain preventive services, such as annual wellness visits and vaccinations. This ensures that you can maintain your health and prevent potential illnesses.

Pros and Cons of Medicare Plan N

Like any healthcare plan, Medicare Plan N has its trade-offs. Here’s a closer look at the advantages and potential drawbacks.

1. Comprehensive Coverage: Plan N offers comprehensive coverage for a wide range of healthcare services, giving you peace of mind knowing that your medical expenses are covered.

2. Affordability: Compared to other Medicare plans, Plan N is often more affordable, making it an attractive option for individuals on a budget.

3. Freedom to Choose Providers: With Plan N, you can choose your own healthcare providers, ensuring you receive care from trusted professionals.

Trade-Offs of Medicare Plan N

1. Out-of-Pocket Costs: While Plan N covers significant healthcare expenses, you’ll still be responsible for out-of-pocket costs, such as the Part B deductible and excess charges.

2. Limited Coverage for Travel: If you frequently travel outside the United States, Plan N may not provide coverage for medical services obtained abroad.

3. Cost-Sharing Requirements: Plan N requires paying copayments or coinsurance for certain services, which can add up over time.

Overall, Medicare Plan N offers comprehensive coverage at an affordable price, making it a popular choice for many individuals. However, it’s essential to carefully consider your healthcare needs and budget before deciding.

Overview of Medicare Plan G

Overview of Medicare Plan G

Medicare Plan G is another option worth considering if you want comprehensive coverage with minimal out-of-pocket costs. This plan is similar to Plan N in terms of coverage, but it has a few key differences that may make it a better fit for certain individuals.

With Medicare Plan G, you have access to the same wide range of benefits, such as hospital stays, doctor visits, and preventive care. Like Plan N, Plan G also has a cost-sharing structure, which requires you to pay the Part B deductible, which is currently $226 annually.

Once the deductible is met, Plan G provides full coverage for Part B services. You pay nothing more. You do not pay the Part B Excess charges. There are no copays for doctor visits or emergency services.

Pros and Cons of Medicare Plan G

Like Medicare Plan N, Plan G has its own set of pros and cons. Here’s a closer look at what you can expect.

1. Comprehensive Coverage: Plan G offers comprehensive coverage for a wide range of healthcare services, giving you peace of mind knowing that your medical expenses are covered.

2. Minimal Out-of-Pocket Costs: Plan G provides complete coverage for Part B services once you meet the Part B deductible, leaving you minimal out-of-pocket costs.

3. Freedom to Choose Providers: With Plan G, you can choose your own healthcare providers, ensuring you receive care from trusted professionals.

Cons of Medicare Plan G

1. Part B Deductible: Plan G requires you to pay the Part B deductible out of pocket. However, once this deductible is met, your out-of-pocket costs are significantly reduced.

2. Potentially Higher Premiums: Plan G may have higher premiums compared to other Medicare plans. However, the comprehensive coverage and minimal out-of-pocket costs may outweigh the higher premium costs for many individuals.

3. Limited Coverage for Travel: Similar to Plan N, Plan G may not provide coverage for medical services obtained outside the United States.

When deciding between Medicare Plan N and Plan G, it’s important to consider your personal healthcare needs, budget, and preferences. Both plans offer comprehensive coverage, but the cost-sharing structure and coverage for the Part B deductible may be deciding factors for many individuals.

Key Differences between Medicare Plan N and Plan G

Key Differences between Medicare Plan N and Plan G

While Medicare Plan N and Plan G cover the same services, and both require you to pay the Part B deductible (currently $226), the other cost-sharing and the monthly premiums differ.

Here are factors to consider:

There is a noticeable difference in premium between Plan N and Plan G. Most of my clients are in the Omaha, Lincoln, and Council Bluffs Metro areas. Looking at the difference in premiums between Plan N and Plan G here, the price range is between $40 to $50 per month (or $460 to $600 per year) more for Plan G than Plan N for a 65-year-old.

The price range for a 75-year-old is $45 to $55 on average (or $540 to $660 per year) more, and an 85-year-old has a premium range of $60 to $80 per month (or $720 to $960) more for Plan G than Plan N.

These premium differences are for Medicare Supplements in the low range of supplements. For higher-priced Medigap policies, the range is even wider.

Why Is Medicare Plan G Premium More Than Plan N?

Depending on your age, you pay $540 to $960 more per year for a Plan G over a Plan N Medicare Supplement. Why?

There are a number of reasons.

- You don’t pay the $20 copay for doctor visits on Plan G. The plan pays the cost, and it is reflected in the premium.

- You don’t pay Part B Excess Charges on Plan G. The plan pays the cost, and it is reflected in the premium.

- You don’t pay the $50 copay for emergency room services on Plan G, and it is reflected in the premium.

- Plan G is the most popular Medigap Plan and the default guarantee issue plan.

How Should I Compare Medicare Plan N to Plan G?

Copays

Copays

How many times would you have to go to the doctor for Plan N to be more expensive than Plan G? The answer is to divide the $20 doctor copay into the annual price difference–$540 premium / $20 copay = 27 doctor visits. For a 65-year-old, you would need to go more than 27 times for Plan N to cost you more than Plan G. That is a lot of doctor visits! How many times do you go to the doctor each year normally? Once, twice, five times?

Medigap Plan N has an emergency room maximum copay of $50. You will probably not go to the emergency room regularly or for prolonged periods. If you go to the emergency room frequently, I guarantee it will NOT be for a prolonged period. We can eliminate the $50 emergency room copay as seriously impacting your total annual cost.

Medicare Part B Excess Charges

Most doctors who are contracted with Medicare do not charge the Part B Excess Change. Of the 2% of doctors who do, they are in mental health and podiatry.

You have control of these charges by asking the physician ahead of time if she takes assignment for Medicare. In other words, does she accept what Medicare bills and does not charge the excess?

Medicare Plan N vs Plan G Rate Increases

Healthcare costs go up. In our current inflationary environment, those increases will be substantial. The insurance companies cover increased costs with rate increases. Your monthly premium will go up in the near future, and if you wish to keep your policy, you must pay the increased cost.

In general, the rate of increase for Medigap Plan G is higher than for Plan N. The difference ranges from 1% to 4% over time and from state to state and company to company, but the rate increases are usually more for Plan G than Plan N, as a rule.

Medigap Plan G Is More Popular

Plan F is still the most popular, with 46% of Medigap policyholders enrolled in Plan F. However, that is quickly decreasing because beneficiaries who turn 65 after 2020 are no longer eligible to purchase Plan F.

Plan G is the most comprehensive Medigap plan because all health issues are paid for after the $226 Part B deductible is met. Like Plan F before, Plan G is the go-to plan for the majority, with 26% currently enrolled in Plan G versus Plan N at 10%.

Medigap Plan G Is Guarantee Issue

After someone’s Initial Enrollment into Medicare at age 65 or when they enroll in Medicare Part B, most people must go through underwriting to get Medicare Supplements. They must answer a series of health questions, and the insurance company can determine whether to accept them into the policy, accept them at a higher premium, or decline them.

There are a handful of exceptions to this rule. Insurance companies must guarantee to issue a Medigap policy when someone comes off a Medicare Advantage plan in their first year on the plan. The other most common instance is when a person has Medicare Part A and Part B, losing their group health plan. Then, they can get a Medigap plan without answering health questions, in other words, guaranteed issue.

The vital point about guaranteed-issued policies is that Plan G is the only plan eligible for the guaranteed issue. Insurance companies cannot screen guarantee issue applicants. They must take them no matter their health. Coupled with the fact that Plan G is now the most popular plan, Plan Gs have a disproportionately large number of unhealthy participants vs Plan N.

Consequently, the Medicare Plan G member pool has proportionally more medical claims than Plan N policies. The higher claims ratio increases the costs for Plan G vs Plan N. The higher costs result in high average annual rate increases between Medicare Plan G vs Plan N. Medicare Plan G rate increases average between 1% to 4% more each year. Over time, there is a significant difference in what a beneficiary pays for their Medigap Plan G vs Plan N.

Rate Increases Are Lower for Plan N

Rate Increases Are Lower for Plan N

For example, if a Medigap Plan G $150 premium at 65 increases by 4% on average for fifteen years, the premium will be $270 at 80. If a Medigap Plan N $110 premium at 65 increases by 2% on average for fifteen years, the premium will be $148 at 80.

The Medicare Plan N premiums are smaller than Plan G, but Plan G premiums more than double in the same time period because of the higher percentage increase and larger initial premium.

While the Plan N $20 doctor copays and the $50 emergency room fee are essential to remember, the smaller percentage increase in annual cost for a Plan N is the real underlying factor to weigh when deciding about your Medicare coverage. Plan G’s percentage increase, because of its popularity and guarantee issue status, ensures you will probably pay significantly more for Medicare Plan G than Plan N over time.

The Bottomline: Medicare Plan N vs Plan G

Choosing the right Medicare plan is crucial and can significantly impact your healthcare and financial well-being. Medicare Plan N and Plan G are excellent options for individuals seeking comprehensive coverage, but it’s important to understand their differences.

Choosing the right Medicare plan is crucial and can significantly impact your healthcare and financial well-being. Medicare Plan N and Plan G are excellent options for individuals seeking comprehensive coverage, but it’s important to understand their differences.

In this comprehensive guide, we’ve explored the coverage details, benefits, pros, and cons of Medicare Plan N vs Plan G. We’ve also discussed the key differences between the two plans and provided factors to consider when deciding.

By evaluating your healthcare needs, budget, and preferences, you can choose the Medicare plan that provides the best coverage for you. Whether you opt for Medicare Plan N vs Plan G, both plans offer comprehensive coverage and the peace of mind that comes with knowing your medical expenses are taken care of.

Medicare Plan G offers the convenience of comprehensive coverage. Once your small Part B deductible of $226 is met for the year, you don’t have to worry about any further out-of-pocket expenses for your health coverage. The tradeoff, however, is you pay for that convenience, especially over time in higher premiums and consistently higher rate increases that may strain your fixed budget as it is eroded more and more by inflation or other unplanned expenses.

Medicare Plan N gives you the same coverage, but you will be responsible for minimal doctor and emergency room copays. Those copays, while they may

Christopher J. Grimmond

seem to be a nuisance, keeping a lid on the rising cost of healthcare coverage. Your premium may be more palatable ten and fifteen years down the line.

Hopefully, you will be on Medicare for a long time. Weigh carefully the costs and tradeoffs over the next fifteen or more years.

We can help you sort through the confusion that is called Medicare and the seemingly endless number of Medicare Supplements and Medicare Plans at no cost to you. Call us at 402-614-3389 and speak with an experienced and licensed insurance agent professional.

When people arrive at the doorstep of Medicare at age 65, they are confronted with the daunting task of picking a Medicare plan. Most people find picking Medicare plan overwhelming and confusing.

100’s of Supplements to Pick From

Insurance companies offer hundreds of different Medicare supplements, Medicare Advantage plans, and Medicare Part D prescription drug plans. Picking Medicare plan means choosing between Medicare supplements and a Part D prescription drug plan OR Medicare Advantage/Part C. Next picking Medicare plan means choosing the plan type. Medigap plans range from plan A through the alphabet to plan N, which doesn’t include a Part D drug plan. The drug plans can be a little simpler because you can use the Medicare tool to narrow down the selection. The Medicare calculator bases the plan selection upon the prescriptions you enter into the system. The calculator picks the Medicare Part D plan that will cost the least in total costs for you. On the other side, Medicare Advantage plans consist of a wide variety of co-pays, co-insurance, deductibles, and maximum out-of-pocket costs and amounts that may or may not include a Part D plan.

Foreign Language of Medicare

Medicare itself is like a foreign language of Part A, Part B, and Part D with rules around enrollment that includes penalties when you do not comply. The Medicare.gov website is meant to be helpful, but the shear amount of information, jargon, legalese makes it a barrier to entry rather than a door. Even the Medicare handbook is hundreds of pages. Its size makes the evaluation of information almost impossible.

The Pain of Picking Medicare Plan

The Pain of Picking Medicare Plan

As a consequence, picking a Medicare plan is a frustrating and painful process for people. That is why I take people through a 3-step process. 1.) There is a brief, foundational explanation of Medicare and how it works. 2.) Look at ALL of the plans, but in an organized and ordered fashion. The first step helps you evaluate the plans. I share the story behind each company from my fifteen years of insurance experience because each company has a history in the market. 3.) I find out about you. Everyone is unique. Some people are risk takers. Others are not. Some have health concerns that are foremost of mind. Others do not have any.

Logical Process

The logic of the process enables people to narrow down choices and make the best one for them. I ask questions as we go along. Test and probe. Explain aspects of the plans as we go through each. Constantly test for understanding. So the process of picking a Medicare plan becomes clearer as we move through it. I generally meet with people twice. The first time is usually months before they can do anything. There is no pressure to make a decision or ‘buy right now.’ Clients have time to think, collect more information, verify what they’ve learned, talk with confidants. The next time we get together is to review with updated information. That is the time for picking a Medicare plan. By then you are comfortable and confident with your decision because your decision is well informed. It is logical. The decision is made over time without pressure. You know what you are doing when you pick your Medicare plan.

If you would like to go through this process, there is not cost or obligation. Call 402-614-3389 to find out more.

Medicare Changes Part B Deductible

Medicare changes came out in December. The Medicare changes Part B deductible was an increase. The Medicare Part B deductible for 2016 was $166. The 2017 Part B deductible is $183. While the $17 increase is small in dollar terms, it was a 10% increase. That’s big!

Part B Deductible

Part B Deductible

What is the Medicare Part B deductible? Medicare Part A and Part B have various deductibles and co-insurance costs that you pay. While Medicare covers the majority of medical cost, you have some significant responsibility, especially if there are frequent and/or high dollar medical need. Part B covers doctors visits and outpatient procedures, which is everything other than the hospital. Medicare will cover 80% of those costs. Your portion is 20%, but before the 20% starts, you have an annual deductible. The key to the Part B deductible is that it is an annual deductible. You pay the Part B deductible only once per year, which is different from the Part A hospital deductible.

Plan G Vs. Plan F

Medicare Supplement Plan G is becoming the most popular supplement plan available. Plan G covers all the Medicare Part A deductibles and Part B co-insurance EXCEPT the Medicare Part B deductible. You pay that directly to the provider after the Medicare discount. Once that is satisfied for the year, you pay nothing else out of pocket.

Medicare Supplement Plan G is becoming the most popular supplement plan available. Plan G covers all the Medicare Part A deductibles and Part B co-insurance EXCEPT the Medicare Part B deductible. You pay that directly to the provider after the Medicare discount. Once that is satisfied for the year, you pay nothing else out of pocket.

You may ask, ‘why don’t I do Plan F where the Part B deductible is also covered?’ If you were on a Plan F, your monthly premium would include the cost of the Part B premium and the increase. You also would pay a substantial fee to the insurance company for them to write the check for $183 for you. By being on Plan G as opposed to Plan F, you avoid the sizeable annual increase and the additional fee for paying the Part B deductible.

While the Medicare changes Part B deductible was not large in dollar terms, the reality is the cost of Medicare will continue to rise along with all medical costs. It is important to have an agent who can help you understand your plan and find the plan that best fits your needs at the lowest cost. Give us a call at 402-614-3389 for a free evaluation.

What is Medicare? A basic question. Or rather, why should anyone care about Medicare? The reason people should care is that most bankruptcies are medical bankruptcies. In other words, if you wish to protect your retirement nest egg from bill collectors, Medicare is important to know about. There are few things that are more disturbing than a pile of medical bills sitting on the kitchen table. The golden years could be tarnished with worrying about actual or potential medical expenses. Medicare–if implemented proper–will protect you from a potential catastrophe. It is critical for people entering into retirement to understand what is Medicare.

What is Medicare?

Medicare is a Federal health insurance program for people who are 65 and older (or on Social Security disability). It began in 1965 when President Johnson signed it into law. It was designed to provide medical covered to the elderly at a reasonable price. In 1965, few people had health coverage once they stopped working. As a result, many seniors fell into poverty because of burdensome medical expenses. Medicare was a solution to a national problem.

Medicare is a Federal health insurance program for people who are 65 and older (or on Social Security disability). It began in 1965 when President Johnson signed it into law. It was designed to provide medical covered to the elderly at a reasonable price. In 1965, few people had health coverage once they stopped working. As a result, many seniors fell into poverty because of burdensome medical expenses. Medicare was a solution to a national problem.

Medicare Part A

Medicare is divided into two parts: Medicare Part A and Medicare Part B. Medicare Part A has everything to do with the hospital. It doesn’t cost anything because you paid for it during your working years. It was one of the deductions in your payroll taxes. Medicare Part A covers a 100% of the medical expenses incurred in the hospital, but there is deductible that many people are not aware of. The Medicare Part A deductible is currently $1,288. This is NOT an annual deductible. It is a deductible per benefit period, and a benefit period is 60 days. So each event has a deductible, and the time for the event is 60 days. In other words, you could have multiple events and pay multiple deductibles because the event is not limited to just a 60 day period. Each new event, even if it overlaps with another event, has its own 60 day timeline. While rare, it could happen, and probably more importantly, you could pay the Part A $1,288 deductible more than once in any given year.

Medicare Part B

Medicare Part B, however, does cost something. For most people going on Medicare and Social Security in 2016, the Medicare Part B premium is $121.80 per month. It is generally taken out of your Social Security check. Medicare Part B covers doctors’ visits and outpatient procedures, such as X-rays, blood work, emergency room visits, etc. Medicare Part B covers 80% of the cost. Your portion is 20%. The 20% coinsurance, however, is unusual. There is no cap. There is no maximum out-of-pocket. Most group plans you were ever on probably had a maximum out-of-pocket. It may have been $1,000, $2,000, even $10,000, but at some point, you stopped paying and the insurance company covered everything. Medicare Part B does not have that, so 20% of a big number will be a big number. You keep paying your 20% coinsurance as long as the bills come in.

These are the basic building blocks to what is Medicare. You must understand Medicare, Medicare Part A, and Medicare Part B to understand the rest that follows. In the next blogs and videos, we will cover how to get Medicare, how to cover the Part A deductible, and how to fill the unlimited 20% gap in Part B coverage.

Delay Medicare Enrollment

Many people work past 65. They continue on with them employer group coverage. They delay Medicare enrollment. At 66+, they wonder what to do about Medicare.

How to Enroll after 65

Here is what to do. Go to Medicare.gov. Click on “Forms, Help, Resources” on the top right. Then click on “Medicare Forms” on the left middle. You will see the enrollment forms in the middle of the page in PDF form. There are two forms: one to enroll in Medicare Part B and a second for your employer to sign off on your coverage. You fill out the enrollment in Part B. Give the second form to your employer. Your employer will verify that you have had health coverage as good as Medicare since you turned 65. They will sign the form. It is important for you to write in the date that you wish your Medicare Part B to start. Give yourself enough time to find a Medicare plan and prescription drug plan. (There are much shorter and restrictive time limits when you have delayed Medicare Part B enrollment.) Drop the forms in the mail or hand deliver them to the local Social Security office.

Medicare Employer Enrollment Forms

Why do you want to involve your employer with your enrollment in Medicare Part B? If you do not have your employer verify that you had health coverage from the time you could have enrolled in Medicare until the time you did take Part B, Medicare will assume you did not have creditable coverage and will asset a penalty. The penalty is a 10% increase in Part B premium for every year you did not have coverage. That can be significant over time and completely unnecessary. Delay Medicare enrollment at your own risk. Get the form. Your employer is required to verify. The human resource department will know exactly what to do. It is a very simple matter.

At Omaha Insurance Solutions, we help clients who delay Medicare enrollment all the time. We can get this done quickly and easily. Give us a call 402-614-3389. We can email you the forms, walk you through filling them out, and explain what to do.

A distressed prospective client told me that Medicare did not cover mental health treatment. I stammered a bit because the subject had never come up before, and I was surprised. I said that it did. She had read that it only covered a one time welcome visit to Medicare. I then showed her in the Medicare & You Handbook on pages 40 and 59 where it detailed the coverage. There is the welcome to Medicare screening, an annual screening, and complete medical coverage. She was surprised and relieved there was Medicare mental health care.

Seniors Need Mental Health Care

Mental health is a serious problem in society, and it is growing among seniors. The World Health Organization documents how important among seniors this issue is. Depression is under reported, little recognized, and often an untreated illness; but Medicare mental health cares for beneficiaries with mental health concerns, like depression. It probably does it better than most employer plans do.

Medicare Mental Health Part A

Medicare Part A deals with the hospital. The same rules around hospital deductibles and co-insurance apply to psychiatric hospitals as to other hospitals. There is, however, one difference. Medicare only allows a lifetime amount of 190 days for a stand alone psychiatric hospitals.

Medicare Mental Health Part B

Medicare Part B covers psychiatrists, counselors, treatment groups. Again the same 20% co-insurance applies as to any other Part B doctor visit. If you have a long standing relationship with a psychologists before Medicare, you may keep that relationship going after you go on Medicare if the medical professional takes assignment for Medicare.

Medicare Supplements will cover Medicare mental health issues and professionals the same as other fees in accordance with your particular Medicare supplement plan. Medicare Advantage will have the same co-pays for psychiatrists and psychologists as for other specialists.

No need to be stressed or depressed about Medicare mental health. You are covered.

A gentleman called me who was losing his group health coverage from a former employer. He was a retiree from a Fortune 100 company. You would recognize the name of the company immediately. As part of his retirement package, he had a very generous health plan for himself and his wife. He had been on it for decades, but the company could no longer afford to maintain it. They canceled the plan, so my client found himself cast out into the Medigap world at 92 not knowing what to do, and he didn’t realize that he would need a Medigap guarantee issue to be get a plan.

Medigap Guarantee Issue Solution

When you are a Medicare beneficiary and you loss group coverage, you have what is called a guarantee issue period. It is a very limited opportunity that has an exasperation date on it. It is an incredibly important guarantee for those who have pre-existing conditions.

What is Medigap Guarantee Issue?

What is guarantee issue for a Medigap policy? How does it work? What should you do to make sure you don’t miss out? Guarantee issue for a Medigap policy applies to a number of situations. I will just speak to one—when you involuntarily lose your group health coverage while on Medicare Part A & B. Guarantee issue means that an insurance company must offer you a Medigap plan—usually plans A, B, C, & F—without asking health questions. They must sell it to you no matter your health condition. For those with pre-existing conditions that would exclude them, this is a treasure. (Each state may handle guarantee issue situations somewhat differently, but this is the general concept.)

How Does Medigap Guarantee Issue Work?

How Does Medigap Guarantee Issue Work?

How does guarantee issue work for a Medigap policy when you have involuntarily lost your group health coverage? The company that is ending group health coverage will usually give you sufficient time to find other coverage. You are able to purchase a supplement as early as 90 days ahead of time. After coverage has ended, you usually only have 63 days to find coverage without going through underwriting. If you miss that time frame and you have a serious health issue, you will not find a Medigap policy. You will only have Medicare.

What Should You Do to Get Your Medigap Guarantee Issue?

What should you do if you are losing your group plan that covers your Medicare deductibles and coinsurance? First get educated about Medicare. Second get a quote and start looking for a Medigap plan. Third see if you can pass underwriting so you are not restricted to the more expensive plans, but please don’t doddle. There is a clock ticking in terms of your guaranteed issue period.

To summarize, you have a special opportunity to get a Medigap plan when you lose your group plan. The special opportunity is that you do not have to answer health questions for a defined period and the insurance company has to sell you a plan. You need to be aware of the rules and follow them so you do not miss out. Still try underwriting so you have more options, but you have the guarantee provision to fall back on. There are rules and time limits around guaranteed issues. Make sure you fully understand these rules and the ramifications. Call to find out the facts so you don’t miss out. 402-614-3389 OmahaInsuranceSolutions.com

I quoted a prospective client a Medicare supplement rate that was significantly less than the plan he was currently on. When I explained that he would have to go through Medicare supplement underwriting and answer some health questions because he was no longer in his Open Enrollment, he wasn’t happy.

Why was he upset? Because he remembered how time-consuming and intrusive it was to apply for life insurance. A nurse came to his home, weighed and measured him, took blood and urine, and asked a bunch of questions. Then, they got reports from the various doctors and a letter about a certain health issue.

The client claimed there was no amount of money that could induce him to go through all again. That’s understandable. However, when I said I could probably do the Medicare supplement underwriting in sixty seconds or less, his tone changed.

How can Medicare supplement underwriting be so simple, though? Let me explain.

Medicare Supplement Underwriting

How is Medicare underwriting defined in Omaha? In short, it’s a simple process used by insurance companies to learn more about you and your health. There’s no need for medical exams or doctor’s visits – all you’re doing is answering a basic set of health questions.

What are the Health Questions for Medicare or Medigap Supplement Underwriting?

The questions can be grouped broadly into four categories:

- Knock-out questions

- Height and weight

- Current health issues

- Smoking status

If you answer “yes” to certain knock-out questions, then you can’t get Medigap or a Medicare Supplement – here’s how it works.

Medigap Underwriting Questions: What Are Knock Out Questions?

They are questions relating to serious medical conditions. If you have this serious medical condition, you are ineligible for a Medicare supplement or “knocked out” of consideration.

To clarify, you can’t be denied Medicare, but a private insurance company can deny coverage for a supplement outside of your Open Enrollment Period.

What are some examples of knock out questions? They vary, but they include:

- Are you currently confined to a wheelchair, nursing facility, or hospital bed?

- Do you currently receive assistance bathing, transferring, toileting, eating, dressing or need the assistance of a walker?

- In the last two years, have you received treatment for cancer, leukemia, heart attack, congestive heart failure, multiple sclerosis, chronic kidney disease, diabetes with hypertension, stroke, etc.?

Why Does Medicare Ask Questions About Height and Weight?

The second category of questions has to do with height and weight. This is always a difficult question. If I asked my wife her weight, it would be very quiet and cold in the Grimmond household for a while. However,height and weight is an important determiner of future health, so it has an impact on price.

What Are Current Medical Issues?

Current issues cover existing medical conditions and related future treatment. For example, you may have a diagnosis for a future treatment, like a knee replacement or cataract surgery.

For Medicare supplement underwriting purposes, you’ll probably need to address these medical issues before you can change supplements or the insurer simply won’t cover that procedure for the first six months.

You may have had respiratory issues in the past that do not exclude you now, but if you are currently being treated for the issue, they could prevent you from getting the supplement for a time.

Why Am I Asked About Smoking Status?

There is plenty of medical evidence about the health risks associated with smoking, which also includes chewing.

I met with a gentleman who described himself as a non-smoker, but when I pointed out he had a circle print on his back jeans pocket, he fessed up that he dipped occasionally. In medical underwriting, even occasional dipping means you’re still considered a tobacco user.

Smoker/Non-smoker is the one health question that can be asked during Open Enrollment.

Medicare Supplement Underwriting is Easy

Why does this matter to you? Because your answers determine whether the insurance company accepts or denies you. It determines your health category and consequently your monthly premium. Underwriting is not a difficult or a daunting task with a skilled insurance agent such as myself. It just takes a few minutes of your time, and you may be able to save yourself some money and maybe improve your coverage as well.

Medicare Supplement Underwriting Omaha Insurance Solutions

The key thing to understand is that not all insurance companies have the same underwriting guidelines. Some may be laxer or more restrictive than others. They may be lenient on one condition or more severe on another. That is when an experienced agent can help you with getting the best outcome for your underwriting. He can guide you to the company that will be most favorable to your condition for the best possible price.

Call OmahaInsuranceSolutions.com 402-614-3389 for help with your Medicare Supplement underwriting in Nebraska

A prospective client called me about saving money on her Medicare supplement. I asked her the basic supplement health questions and gave a quote. We set up a time to meet. At the meeting, I started going through the standard health questions on the application. When I came to the question about recommended future treatments, she said no, but the way she answered bothered me. So I asked it a different way. “Did the doctor suggest that you have anything done, like cataract surgery, knee or hip replacement?” Then she lit up. “My hips are really bad,” she said. “He thinks I should replace them sometime.” “So when you say sometime, are you talking about in a year or two?” “Oh no,” she said. “In the next couple of months.” I closed my notebook. We were done.

Supplement Health Questions Broken Down

Recommended treatments by a physician could potentially cause a problem when you switch supplements. Three things to know: 1.) what is a recommended treatment, 2.) why does it matter, 3.) what should you do about it.

Most of the time when we see the doctor it is because we are sick right now. She makes a diagnosis and recommends an immediate treatment. ‘Take this pill now.’ ‘Have open heart surgery next week.’ Sometimes the diagnosis leads to a recommendation for treatment sometime in the future. ‘Your knees are deteriorating. You should have a knee replacement in the next year or so.’ When your doctor puts a recommendation in your medical records for a future treatment, that is a big deal. To an insurance company, that means there will be a future big bill for whoever is insuring you at that time.

Understand the Supplement Health Questions

The problem is that you could get stuck with the bill instead of the insurance company if you don’t follow the rules. If you have something done that was recommend before you got the new policy, like cataract surgery within six months after getting a new Medicare Supplement, the insurance company will probably not pay their share of the expense. The health questions in the application are designed to disclose recommended treats and prevent the new insurance company from getting stuck with the bill. They would likely refuse payment and call for doctor’s records to see if there was a recommendation for treatment before you signed the application. After six months, you are less likely to have any trouble. They cannot hold back paying for treatment indefinitely. The bottom line is, if you have any recommended treatments, finish them up before switching supplements.

The problem is that you could get stuck with the bill instead of the insurance company if you don’t follow the rules. If you have something done that was recommend before you got the new policy, like cataract surgery within six months after getting a new Medicare Supplement, the insurance company will probably not pay their share of the expense. The health questions in the application are designed to disclose recommended treats and prevent the new insurance company from getting stuck with the bill. They would likely refuse payment and call for doctor’s records to see if there was a recommendation for treatment before you signed the application. After six months, you are less likely to have any trouble. They cannot hold back paying for treatment indefinitely. The bottom line is, if you have any recommended treatments, finish them up before switching supplements.

Manage the Supplement Health Questions

This problem, of course, can be avoided. Check with your doctor. See if he is recommending any treatments and see if he put that in your medical records. Check with the insurance company if you recently switched supplements. Doctor’s offices will not usually check with an insurance company on a supplement because they will assume the insurance company will pay when Medicare pays. If you recently switched supplements, call and ask ahead of time if there will be any issues about a procedure. It is always good to cross your T’s and dot your I’s when it comes to new insurance plans.

This problem, of course, can be avoided. Check with your doctor. See if he is recommending any treatments and see if he put that in your medical records. Check with the insurance company if you recently switched supplements. Doctor’s offices will not usually check with an insurance company on a supplement because they will assume the insurance company will pay when Medicare pays. If you recently switched supplements, call and ask ahead of time if there will be any issues about a procedure. It is always good to cross your T’s and dot your I’s when it comes to new insurance plans.

Ask an Expert about Supplement Health Questions

A mistake around a recommended treatment when changing Medicare supplements could result in bills to you for thousands of dollars. Know whether you have any recommendations from a physician for future treatments in your records. Understand what that means in relationship to a new Medicare supplement. Talk with someone who can ask you the right questions when you are making a change to your supplement coverage 402-614-3389. OmahaInsuranceSolutions.com

For two years, my father was on dialysis. Those were tough years. When I got a client on dialysis, I wanted the best for him. Kidney dialysis is one of the pre-existing conditions that usually excludes you from a supplement. My client had a one-time opportunity. I was going to make sure he got it!

Obama Care Confuses Pre-Existing Conditions

![]() Pre-existing conditions are confusing when it comes to Medicare. The ACA (Affordable Care Act) a.k.a. Obama Care made it more confusing because ACA covers pre-existing conditions, but ACA is not Medicare. Different rules govern Medigap policies. ACA applies to everyone 64 and younger. Medigap policies are for everyone 65 and older.

Pre-existing conditions are confusing when it comes to Medicare. The ACA (Affordable Care Act) a.k.a. Obama Care made it more confusing because ACA covers pre-existing conditions, but ACA is not Medicare. Different rules govern Medigap policies. ACA applies to everyone 64 and younger. Medigap policies are for everyone 65 and older.

Medicare Has No Pre-Existing Conditions

Medicare itself cannot deny coverage to anyone because of pre-existing conditions. Medicare means Original Medicare. Original Medicare is Medicare Part A for hospital and Part B for doctors and outpatient. Medicare Part D cannot be denied for pre-existing conditions no matter the condition or cost of the medications. Medicare Part C (or Medicare Advantage) must accept you as well, but for one exception–ESRD (End Stage Renal Disease). You can be denied entrance to Medicare Advantage if your kidneys are permanently shut down and you are on dialysis. All Medicare beneficiaries may enroll in a Medicare Advantage plan, except for that one pre-existing condition.

Medigap Has Pre-Existing Conditions–Sometimes

An insurance company, however, can deny you a Medicare Supplement/Medigap plan because of pre-existing conditions, except during your Open Enrollment Period or Guaranteed issue. The rules around your Open Enrollment Period are confusing. You can enroll in Medicare when you turn 65 and enroll in Medicare Part B. That is called your Open Enrollment. The time period for that is 3 months before the month of your birthday, the month of your birthday, and 3 months after your birthday. The same term–Open Enrollment–is used for enrolling in a Medicare supplement, but the time period is different. Open Enrollment for a supplement is from the month of your birthday and five months after. Same term–Open Enrollment Period–but different time periods that apply to different things. Isn’t that nice!

An insurance company, however, can deny you a Medicare Supplement/Medigap plan because of pre-existing conditions, except during your Open Enrollment Period or Guaranteed issue. The rules around your Open Enrollment Period are confusing. You can enroll in Medicare when you turn 65 and enroll in Medicare Part B. That is called your Open Enrollment. The time period for that is 3 months before the month of your birthday, the month of your birthday, and 3 months after your birthday. The same term–Open Enrollment–is used for enrolling in a Medicare supplement, but the time period is different. Open Enrollment for a supplement is from the month of your birthday and five months after. Same term–Open Enrollment Period–but different time periods that apply to different things. Isn’t that nice!

During your Open Enrollment Period for a supplement, the insurance company may not ask you health questions. They must give you the best possible rate. Even your weight is not counted against you if you are a few pounds over the normative height/weight charts. You can be on chemo, dialysis, recovering from a stoke. It doesn’t matter. The insurance company MUST take you during this time period. AFTER the six month Open Enrollment Period, they can ask health questions when you go to purchase a Medicare supplement, and based upon your answers, the insurance company could rate or even deny you.

What are some of the health questions? Are you in a wheel chair? Are you an insulin dependent diabetic? Have you had a heart attack, stroke, or cancer in the past two years? All of these questions are “knock out” questions. If you answer in the affirmative, you will be denied a Medicare supplement. You cannot be denied Medicare, but you can be denied the ability to purchase a Medicare supplement at any price.

What are some of the health questions? Are you in a wheel chair? Are you an insulin dependent diabetic? Have you had a heart attack, stroke, or cancer in the past two years? All of these questions are “knock out” questions. If you answer in the affirmative, you will be denied a Medicare supplement. You cannot be denied Medicare, but you can be denied the ability to purchase a Medicare supplement at any price.

Know the Rules or Find Someone Who Does

The ACA changes that permit acceptance into a health plan with pre-existing conditions created confusion in the Medicare world. Beneficiaries need to clearly understand that a pre-existing condition can count you out of a supplement unless it is your Open Enrollment Period or Guarantee issue situation. It is critical that persons with serious health issues be vigilant about these Medicare rules and/or find someone who will be vigilant for you.

Don’t miss your Open Enrollment Period. If there are any questions, give us a call at 402-614-3389 or even call Medicare 800-633-4227. Make sure you understand the rules that apply to you.

Contact: Omaha Insurance Solutions