Medicare Part DCategory:

Finding effective solutions to manage weight loss can sometimes feel like searching for a needle in a haystack. But what if there was a medication that could help you on your journey? Enter Ozempic, a breakthrough drug making waves in the weight loss community. Does Medicare cover Ozempic for weight loss?

Finding effective solutions to manage weight loss can sometimes feel like searching for a needle in a haystack. But what if there was a medication that could help you on your journey? Enter Ozempic, a breakthrough drug making waves in the weight loss community. Does Medicare cover Ozempic for weight loss?

In this article, we will explore how Medicare may give you access to Ozempic, giving you the insights you need to make informed health decisions. We’ll also explore the eligibility criteria, coverage options, and potential costs. Whether you’re already enrolled in Medicare or considering it in the future, this information is invaluable for those seeking weight management solutions.

What is Ozempic?

Ozempic is a medication used to treat type 2 diabetes in the class of drugs called GLP-1 receptor agonists. As a GLP-1 receptor agonist, semaglutide enhances the effects of the naturally occurring hormone GLP-1, which helps lower blood sugar levels. This medication is administered once weekly via injection, making it a convenient option for those managing diabetes. Ozempic is effective in reducing A1C levels and promoting weight loss in patients.

A 0.25 or 0.5-milligram dose of Ozempic currently retails on the Novo Nordisk website for $935.77 without insurance. However, those with private or commercial insurance who are eligible for a prescription may pay as little as $25. Medicare Part D and Part D copays for Ozempic can be significantly higher, especially if you fall into the Gap (or Donut Hole).

How Does Ozempic Work?

Ozempic works by mimicking the action of a naturally occurring hormone called glucagon-like peptide-1 (GLP-1) in the body. GLP-1 helps regulate blood sugar levels by stimulating insulin release, slowing down digestion, and reducing appetite. By activating GLP-1 receptors, Ozempic helps lower blood sugar levels, decrease appetite, and promote weight loss.

Who Can Benefit from Ozempic?

Ozempic is primarily prescribed to individuals with type 2 diabetes who have not achieved adequate glycemic control through lifestyle changes, such as diet and exercise, or oral diabetes medications alone. It is typically used as an adjunct to diet and exercise to improve blood sugar control.

GLP-1 also impacts weight via two key mechanisms:

- Affects the hunger centers in the brain (specifically, in the hypothalamus), reducing hunger, appetite, and cravings

- Slows the rate of stomach emptying, effectively prolonging fullness and satiety after meals

The net result is decreased hunger, prolonged fullness, and, ultimately, weight loss.

The Benefits of Ozempic for Weight Loss

Ozempic has gained significant attention in the weight loss community due to its potential benefits. Studies have shown that Ozempic can lead to significant weight loss when used with a healthy diet and exercise. In fact, clinical trials have demonstrated that individuals using Ozempic experienced an average weight loss of 5-10% of their body weight over a 26-52 week period. This is a remarkable achievement, considering many individuals’ challenges when trying to lose weight.

In one large clinical trial sponsored by Novo Nordisk, 1,961 adults with excess weight or obesity who did not have diabetes were given 2.4 milligrams of semaglutide or a placebo once a week for 68 weeks, along with lifestyle intervention. Those who took semaglutide lost 14.9% of their body weight compared with 2.4% for those who took the placebo.

Understanding Medicare Coverage

Before we dive into the specifics of Medicare coverage for Ozempic, it’s important to have a basic understanding of how Medicare works.

Medicare is a federal health insurance program primarily designed for individuals aged 65 and older, as well as certain younger individuals with disabilities. It consists of different parts, including Part A (hospital insurance), Part B (medical insurance), Part C (Medicare Advantage), and Part D (prescription drug coverage).

Medicare covers a wide range of medical services and treatments, including prescription medications. However, coverage for prescription drugs can vary depending on the specific plan you have. Some plans may cover a broader range of medications, while others may have more limited coverage. Understanding your specific Medicare plan is essential to determining the coverage options available for Ozempic.

How Medicare Covers Ozempic for Weight Loss

How Medicare Covers Ozempic for Weight Loss

To determine if Ozempic is covered by Medicare for weight loss, you need to check whether it is included in your Medicare Part D plan’s formulary. A formulary is a list of prescription drugs covered by a specific Medicare plan. You can typically find this information in the plan’s drug formulary document, which is usually available on the plan’s website or by contacting customer service.

All 21 Medicare Part D prescription drug plans and all 30 Medicare Advantage plans cover Ozempic in the Omaha, Lincoln, and Council Bluffs areas. Depending on the plan, you may or may not have a drug deductible and then copays. Ozempic is usually a tier 3 medication with a hefty copay. Depending on your total medications, you may or may not go into the Gap (or Donut Hole).

If Ozempic is included in the formulary, it means that it is covered by your Medicare Part D or Part C plan. However, coverage may still be subject to certain conditions. The medication must be medically necessary for the prescribed purpose. Other factors include prior authorization or step therapy.

Prior authorization requires your healthcare provider to obtain approval from the Part D prescription drug plan before prescribing Ozempic, while step therapy may require you to try other medications before Ozempic is covered.

Review the specific coverage requirements outlined in your Medicare Part D plan to ensure you meet all the necessary criteria for Ozempic coverage. It is important to understand Medicare covers Ozempic for diabetic and pre-diabetic treatment. Medicare does not cover Ozempic for weight loss exclusively.

Why Medicare Does Not Cover Ozempic for Weight Loss

Medicare Part D prescription drug plans were created under the Busch Administration. The Medicare Prescription Drug, Improvement, and Modernization Act (MMA) of 2003 determined that Part D prescriptions could not cover medications for cosmetic or weight loss reasons. Thus, Ozempic is only covered by Medicare for type 2 diabetes. Ozempic is not covered by Medicare for weight loss.

Wegovy: An Alternative?

Wegovy is a brand-name version of the drug semaglutide, which is the medication Ozempic in a different dosage. The FDA approves Wegovy as a chronic weight management medication, not for type 2 diabetes, like Ozempic.

Medicare, however, does not cover Wegovy because the drug is for weight loss. Medicare does not cover weight loss medications even though obesity is intimately tied to diabetes and a cause of poor health.

How to Navigate the Medicare Coverage Process for Ozempic

Here are some suggestions for you to navigate the Medicare coverage process for Ozempic.

Here are some suggestions for you to navigate the Medicare coverage process for Ozempic.

Check the Formulary

Look for Ozempic in your plan’s formulary to determine if it is covered. Note any additional coverage requirements, such as prior authorization or step therapy.

Consult Your Healthcare Provider

Diabetes and pre-diabetes are usually related to obesity. Discuss your diabetes or pre-diabetes in relation to your weight loss goals with your healthcare provider. See if Ozempic is a suitable option for you. They can help guide you through the coverage process and provide any necessary documentation.

Prior Authorization or Step Therapy

If your plan requires prior authorization or step therapy for Ozempic, work with your healthcare provider to complete the necessary paperwork and submit it to Medicare for approval.

Those who are type 2 diabetic or pre-diabetic AND overweight may be able to get access to Ozempic for their healthcare needs, which secondarily includes weight loss.

Dangers of Ozempic

Ozempic, however, isn’t safe for everyone. According to the company, people with the following conditions should avoid using Ozempic:

- Pancreatitis

- Type 1 diabetes

- Under 18 years of age

- Pregnant or breastfeeding

- Diabetic retinopathy

- Problems with the pancreas or kidneys

- Family history of medullary thyroid carcinoma (MTC)

- Multiple Endocrine Neoplasia syndrome type 2 (MEN 2), an endocrine system condition

As with any prescription medication, you must consult your doctor or other qualified healthcare provider on whether this medication is safe for you and what dosage is appropriate.

Ozempic Side Effects and Health Risks

There are many side effects of taking Ozempic as a weight loss medication, including

- Gastrointestinal issues like nausea, vomiting, and diarrhea

- Constipation

- Stomach pain

- Headache

- Excessive burping

- Heartburn

- Fatigue

- Flatulence

- Gastroesophageal reflux disease

These most common side effects of Ozempic don’t tend to be dangerous and may dissipate as you grow used to the medication. However, there is potential for more serious adverse effects, such as:

- Vision problems

- Swelling in extremities

- Dizziness or fainting

- Reduced urination

- Rash

- Rapid heart rate

- Swelling of throat, tongue, mouth, face, or eyes

- Problems swallowing or breathing

- Fever

- Yellow eyes or skin

- Chronic upper stomach pain

Wegovy, another brand name for semaglutide, may also cause damage to the retina, suicidal ideation, gallstones, pancreatitis, and acute kidney damage.

Moreover, taking semaglutide can increase the chance of developing thyroid tumors, including medullary thyroid carcinoma. Speak with your doctor if you are experiencing any of the side effects listed above.

“Ozempic Face”

You may have heard about “Ozempic face” as a side effect of GLP-1 drugs, though the term is misleading because this can be a side effect of any GLP-1 drug or any other cause of rapid weight loss.

The rapid loss of fat in the face can cause:

- a hollowed look to the face

- changes in the size of the lips, cheeks, and chin

- wrinkles on the face

- sunken eyes

- sagging jowls around the jaw and neck.

If weight is lost more gradually, these changes may not be as noticeable. However, the faster pace of weight loss that occurs with GLP-1 drugs can make facial changes more obvious.

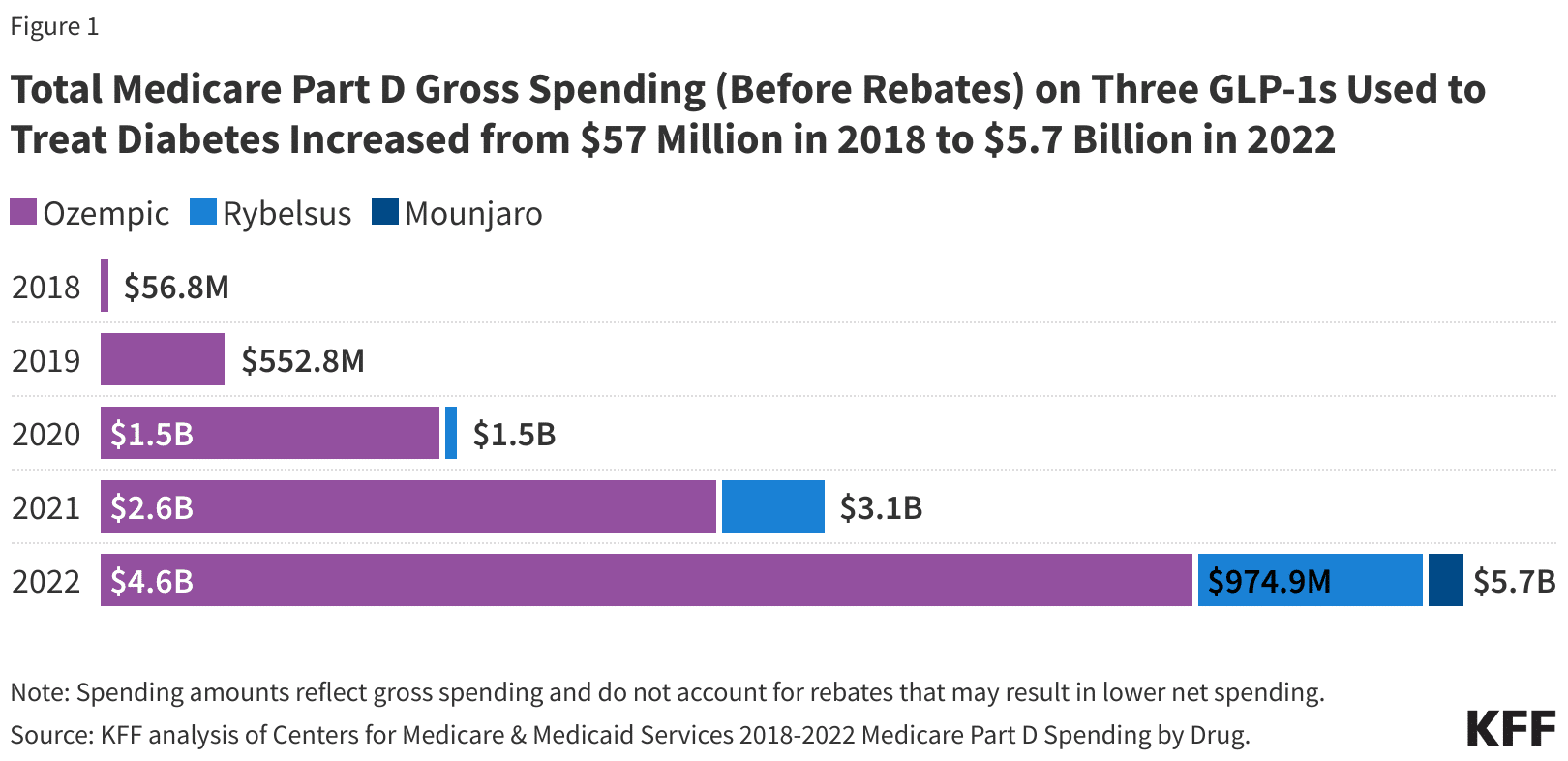

Spending for the three GLP-1 medications, Ozempic, Rybelsus, and Mounjaro, has skyrocketed in the past year on Medicare. While more Medicare beneficiaries are becoming diabetic and using these medications, the number far exceed that type of increase. A significant portion of people on Medicare are now using GLP-1 medications for weight loss.

Medicare Spending on Ozempic Explodes

Impact on Diabetes Patients

The popularity of Ozempic’s off-label use for weight loss is driving a global shortage of diabetes drugs. Pharmacies in the U.S., Canada, and Europe have been reporting shortages. My clients have reported to me their experience of not finding Ozempic at their local pharmacy.

If the shortages persist, people who’ve relied on Ozempic to treat their diabetes may face difficulty adjusting to alternatives. The shortage of Ozempic, driven by its off-label use for weight loss, can have significant consequences for patients with diabetes who genuinely need the medication.

Bottom Line: Medicare Does Not Cover Ozempic for Weight Loss

Ozempic is a dilemma. Most diabetics are overweight, but not all overweight persons are diabetic or pre-diabetic. Medicare does not cover Ozempic for weight loss, but it does cover it for diabetes or pre-diabetes. Weight loss is usually an important element in minimizing the negative effects of diabetes.

While Medicare does not cover Ozempic for weight loss, strictly speaking, Medicare does cover Ozempic for a very large population that also needs and will benefit from Ozempic and losing weight. People aren’t stupid.

It’s actually not a bad solution for an imperfect and overweight world.

Are you confused about Medicare Part D health plans? Don’t worry, you’re not alone. Understanding your options can be overwhelming with all the jargon and complex rules. That’s why we’re here to demystify everything for you.

Are you confused about Medicare Part D health plans? Don’t worry, you’re not alone. Understanding your options can be overwhelming with all the jargon and complex rules. That’s why we’re here to demystify everything for you.

Whether you’re new to Medicare or have been enrolled for years, this article is designed to help you understand the key aspects of Part D plans, including what they cover, how they work, and how to choose the right plan for your needs.

We’ll also answer common questions, such as what medications are covered, how to find the most cost-effective plan, and how to navigate the dreaded coverage gap, known as the “donut hole.”

So, if you’re ready to tackle the confusion surrounding Medicare Part D health plans and take control of your healthcare, let’s dive in and get started.

Who is Eligible for Part D?

Medicare Part D is a prescription drug coverage program the federal government offers to Medicare beneficiaries. Before 2006, there were no government-sponsored prescription drug plans, and the cost of medications was becoming overwhelming for seniors. The Bush Administration introduced a partnership between Medicare and insurance companies known as Part D.

To be eligible for Medicare Part D, you must be enrolled in either Medicare Part A OR Part B. Part A covers hospital stays, while Part B covers doctor visits and outpatient services, but enrollment in either makes you eligible for the Medicare Part D prescription drug benefit.

Medicare Part D health plans are offered by private insurance companies approved by Medicare. These plans are available as standalone prescription drug plans (PDPs) or as part of a Medicare Advantage plan (Part C), which offer additional benefits beyond prescription drug coverage. You must have both Part A and Part B to be eligible for Part C.

Coverage Options and Costs Under Medicare Part D Health Plans

Coverage Options and Costs Under Medicare Part D Health Plans

Medicare Part D plans provide coverage for a wide range of prescription medications. Each plan has its own formulary, which is a list of covered drugs. Medicare regulations require the plan to have at least two drugs in each of the categories CMS (Center for Medicare & Medicaid Services) specifies. These formularies are divided into tiers, each with a different cost-sharing structure.

The costs associated with Medicare Part D plans can vary depending on your chosen plan. Several components to consider include the monthly premium, annual deductible, copayments or coinsurance, and coverage gap.

Premiums for Part D plans can vary widely, so it’s vital to compare plans to find one that fits your budget. In addition to the premium, many plans have an annual deductible that you must meet before many drug copays work. Once you’ve met the deductible, you’ll typically pay a copayment or coinsurance for each prescription.

It’s also important to be aware of the coverage gap, also known as the “donut hole.” The gap occurs when you reach a specific spending limit; then, your prescription drug costs increase significantly in many cases. However, the coverage gap is gradually closing, thanks to the Inflation Reduction Act legislation.

How to Choose the Right Medicare Part D Health Plan in Your Area

Choosing the right Medicare Part D plan can seem daunting, but with careful consideration, you can find a plan that meets your needs and budget. Here are some factors to consider when comparing plans:

- Coverage: Look for a plan that covers all essential medications. Each plan has its own formulary, so it’s important to review the list of covered drugs to ensure your prescriptions are included.

- Costs: Consider the monthly premium, annual deductible, copayments or coinsurance, and the coverage gap. Calculate how much you would pay out-of-pocket for your medications under each plan to determine which one offers the best value. The total cost is the critical comparison.

- Network: Check if your preferred pharmacies are in the plan’s network. Some plans have preferred pharmacies where you can get lower copayments or coinsurance.

When we run client’s medications, I am still amazed by the difference in cost from one pharmacy to another.

- Plan ratings: The Centers for Medicare and Medicaid Services (CMS) rates Medicare Part D plans on a five-star scale. These ratings can give you an indication of a plan’s quality and customer satisfaction.

By carefully evaluating these factors, you can narrow down your options and choose a Medicare Part D plan that best fits your needs.

Understanding the Different Tiers and Formularies

Medicare Part D formularies are divided into tiers, with each tier representing a different level of cost-sharing. The exact number of tiers can vary depending on the plan, but most plans have at least four tiers.

Tier 1 typically includes generic drugs and has the lowest cost-sharing. Tier 2 includes more expensive but still generic low-cost drugs. Tier 3 is for preferred brand-name drugs, followed by Tier 4 for non-preferred brand-name drugs. Tier 5 is usually reserved for specialty medications, with higher cost-sharing.

It’s important to note that not all drugs are covered on every plan’s formulary, and the specific drugs included in each tier can vary. Before enrolling in a Part D plan, reviewing the formulary to ensure your medications are covered and understanding the associated cost-sharing for each tier is essential.

My Experience with Medicare Part D Health Plans in Nebraska & Iowa

My Experience with Medicare Part D Health Plans in Nebraska & Iowa

We have over 2,000 Medicare clients at Omaha Insurance Solutions. During the Medicare Annual Election Period (Oct 15th—Dec 7th), we offer an annual review of clients’ plans, especially the medication part of their Medicare plan. Consequently, we run the medications for hundreds of clients through our Medicare Part D health plan software. It performs thousands of calculations and shows the plans in order of least expensive to most for overall cost. The numbers are broken down into various totals and subtotals by months and tiers for premiums and copays.

We put all the data on a big 42-inch screen for the clients to view. The software can easily manipulate the data, so clients can see which plans work best for their mix of medications, which pharmacies give the best pricing, and when and how much they may fall in the Medicare Gap (or “Donut Hole”) over the course of the year, if at all.

You quickly notice patterns after running thousands of simulations of Medicare Part D health plans during Annual Election Period in Nebraska and Iowa. You notice the same four or five plans at the top. Certain pharmacies consistently perform better for certain plans. You see the big differences in which insurance companies and plans are the winners in the new year compared to the previous year. Some inexpensive drugs are no longer covered under certain plans, or the price charged is totally out of proportion to the actual cost. From our experience of running our Part D analysis software for many years and for so many people, we quickly recognize patterns and can advise clients accordingly.

Tips for Saving on Medicare Part D

Prescription drug costs can add up quickly, but there are several strategies you can use to save money with your Medicare Part D plan. Here are some tips to consider:

- Generic drugs: Whenever possible, opt for generic medications. Generic drugs are just as effective as brand-name drugs but are often significantly cheaper.

- Mail-order pharmacy: Some Part D plans offer discounts for using a mail-order pharmacy. Mail-order can be a convenient and cost-effective way to get your medications delivered to your door.

- Medication reviews: Review your medications with your doctor or pharmacist to ensure you’re still taking the most appropriate and cost-effective drugs. They can also identify any potential drug interactions or duplications.

- Extra Help program: If you have limited income and resources, you may qualify for the Extra Help program, which helps cover the costs of prescription drugs.

By implementing these strategies, you can maximize your savings and ensure you get the most value from your Medicare Part D plan.

Common Misconceptions about Medicare Part D

Several common misconceptions surrounding Medicare Part D can lead to confusion and misinformation. Let’s debunk some of these myths:

- Myth: Medicare Part D covers all prescription drugs. Reality: Part D plans have formularies that only cover certain drugs. It’s crucial to review the formulary to ensure your medications are covered.

- Myth: You can switch plans anytime. Reality: You can only switch plans during the annual enrollment period or if you qualify for a special enrollment period.

- Myth: All Part D plans have the same costs and coverage. Reality: Part D plans can vary in terms of premiums, deductibles, copayments, and formularies. It’s important to compare plans to find the best fit.

- Myth: Medicare Part D health plans do not change much from year to year. Reality: Part D plans change, and in some cases, they change a lot.

By understanding these misconceptions, you can make more informed decisions about your Medicare Part D coverage.

Enrolling in a Medicare Part D Plan

Initial Enrollment Period

Enrolling in a Medicare Part D plan is relatively straightforward, but there are specific enrollment periods to be aware of. The Initial Enrollment Period (IEP) is the seven months surrounding your 65th birthday, including the three months before, the month of, and the months after your birthday.

Annual Enrollment Period

If you miss your IEP, you can enroll during the Annual Enrollment Period (AEP), which runs from October 15th to December 7th each year. During this period, you can switch plans or join a Part D plan for the first time.

Special Enrollment Periods

Special Enrollment Periods (SEPs) allow you to enroll outside the IEP or AEP if you experience certain qualifying events. There are many SEP types. One that is very common is when clients move out of their plan’s service area. Clients move and then call us because they have problems getting medications. “Yes, Medicare canceled your plan when you moved out of the area.”

To enroll in a Medicare Part D plan, contact the plans directly, call 1-800-MEDICARE, or call your agent.

If you call an insurance company, they will tell you one of their plans is best for you. They cannot see or sell you the other insurance companies and their plans.

The people you speak with at Medicare don’t work with insurance companies or Medicare plans. They don’t know the plans or how they work. It is like talking to a person who never worked on a car engine, and his only knowledge is from reading a manual and looking at diagrams.

They run the medications you give them through the software. Whatever the software tells them is what they tell you. They have no experience because they have no clients and get no feedback on the advice they are dispensing. There are no consequences to them if they give bad advice. They will never talk to the same person again. They can recommend anything without being held responsible for the advice dispensed. Insurance agents can be held responsible and are.

The Only Way to Get the Information to Make A Truly Informed Choice

I highly recommend working with a trusted and experienced insurance professional who is independent. In other words, an independent agent or broker can show you most or all of the Medicare Part D health plans in your area and the Medicare Advantage plans with prescription drugs. You want to be confident in the person’s knowledge and expertise. Almost anyone can get an insurance license. The person you use should demonstrate knowledge and expertise to you about Medicare and the various insurance plans. They should display reliability. Those are the people to trust. Think about how you pick a doctor.

All Medicare Part D Health Plans and Advantage Plans Are Local

Plans vary from state to state and region to region. At Omaha Insurance Solutions, we are intimately acquainted with the 21 Medicare Part D plans in Nebraska & Iowa, the 30 Medicare Advantage plans in Nebraska, and the 25 Medicare Advantage plans in Iowa. Clients give us daily feedback on how well or poorly the various companies and plans are performing at any given time. We are familiar with our local networks–CHI Health, Nebraska Medicine, Methodist Health Systems, and Bryan Hospital–and other providers. My home is down the street from MD West One. I have had multiple surgeries myself at OrthoNebraska. We know well the Medicare Advantage and Part D plans in Omaha, Lincoln, and Council Bluffs and the doctors and institutions that work with them.

Nebraska, and the 25 Medicare Advantage plans in Iowa. Clients give us daily feedback on how well or poorly the various companies and plans are performing at any given time. We are familiar with our local networks–CHI Health, Nebraska Medicine, Methodist Health Systems, and Bryan Hospital–and other providers. My home is down the street from MD West One. I have had multiple surgeries myself at OrthoNebraska. We know well the Medicare Advantage and Part D plans in Omaha, Lincoln, and Council Bluffs and the doctors and institutions that work with them.

Clients often call us asking for help navigating the customer service bureaucracy when they encounter problems. We constantly hear what is working and not with Medicare Part D health plans in the Omaha, Lincoln, and Council Bluffs areas. We do three-way phone calls with the insurance provider, the pharmacies, and clients to get problems solved. Sometimes, we connect the billing departments of one of the networks with the insurance company and make sure they are communicating correctly so a client is not billed incorrectly.

Unlike the SHIP office or other volunteer organizations that help seniors with Medicare, we find out directly from clients how well Medicare and the Medicare insurance plans are serving them.

Frequently Asked Questions About Medicare Part D

- Question: What medications are covered under Medicare Part D?

Answer: Part D plans cover a wide range of prescription drugs, including generic and brand-name medications. Each plan has its own formulary, so it is essential to review the list of covered drugs.

- Question: How do I find the most cost-effective Part D plan?

Answer: To find the most cost-effective plan, consider factors such as monthly premiums, deductibles, copayments or coinsurance, and the coverage gap. Use the Medicare Plan Finder tool to compare plans based on your specific medications and needs.

Our propriety software sorts through all the plans in your area, confirm the medications on the formulary, lists the copays and premiums, totals the amounts, and reveals the star rating. I believe the information is presented in a much friendlier format than Medicare’s Plan Finder. We perform the service for FREE. Medicare and the insurance companies compensate the agents.

- Question: What is the coverage gap or “donut hole”?

Answer: The coverage gap temporarily increases prescription drug costs after reaching a certain spending limit. However, it is gradually disappearing.

- Question: Can I get assistance paying for my Medicare Part D plan?

Answer: If you have limited income and resources, you may qualify for the Extra Help program, which provides financial assistance to cover the costs of prescription drugs.

Conclusion: The Importance of Understanding Medicare Part D

Medicare Part D health plans play a crucial role in helping seniors and individuals with disabilities afford their prescription medications. By understanding the in’s and out’s of Part D plans, you can make informed decisions about your healthcare coverage and ensure you get the most value from your plan.

Christopher J. Grimmond, MA, CFP

This guide has given you the knowledge you need to demystify Medicare Part D, from knowing what medications are covered to navigating the different tiers and formularies. Remember to review your options, compare plans, and consider cost-saving strategies to maximize your savings.

Don’t let the confusion surrounding Medicare Part D hold you back from taking control of your healthcare. With the right plan and information, you can confidently navigate the world of Medicare Part D and ensure you have access to the medications you need.

If you want assistance and objective analysis of your area’s Medicare Part D health plans, contact us at [email protected] and 402-614-3389. We will provide you with unbiased and free advice on the Medicare plans that will work for you.

Are you wondering if your Medicare Part D plan covers Xarelto? Well, you’re in the right place! This article will unlock the benefits and examine whether Medicare Part D pays for Xarelto.

Xarelto is a widely prescribed anticoagulant medication used to prevent blood clots. It is commonly prescribed for conditions such as atrial fibrillation, deep vein thrombosis, and pulmonary embolism. Xarelto is also a very expensive medication. Even with Medicare insurance, the copays are high, especially in the Gap phase of Part D.

Navigating the intricacies of Medicare coverage can add an additional level of complexity and confusion around prescription drugs.

Medicare Part D is a prescription drug plan offered by private insurance companies approved by Medicare. The program aims to provide affordable access to various medications, but not all drugs are covered. That’s why it’s crucial to understand whether Xarelto is included in the formulary of your specific Part D plan.

I have hundreds of Medicare clients on Xarelto. We run our clients’ medications through our proprietary software to determine the lowest-cost drug plans. We want the plans to have at least a 3-star or higher Medicare rating. Xarelto is one of many high-dollar medications we have had to deal with for over a decade. This article will delve into Medicare Part D coverage details and explain how we find plans that cover our clients’ Xarelto and other costly medications. So, let’s start unlocking the benefits of Medicare Part D and discovering if Xarelto is covered under your plan.

Understanding Xarelto and Its Importance

Understanding Xarelto and Its Importance

Xarelto, also known by its generic name rivaroxaban, is an oral anticoagulant medication that plays a crucial role in preventing blood clots. Blood clots can lead to serious health complications such as stroke, heart attack, or even death. Xarelto works by inhibiting the clotting factors in the blood, reducing the risk of clot formation.

The use of Xarelto is particularly prevalent among individuals with conditions such as atrial fibrillation, deep vein thrombosis, and pulmonary embolism. Atrial fibrillation is an irregular heart rhythm that can increase the risk of blood clots forming in the heart. Deep vein thrombosis occurs when blood clots form in the deep veins of the legs, while pulmonary embolism is a life-threatening condition where a blood clot travels to the lungs.

Given the importance of Xarelto in managing these conditions, individuals must have access to affordable medication. This is where Medicare Part D comes into play, offering coverage for prescription drugs to Medicare beneficiaries. Let’s explore the coverage options under Medicare Part D and how they relate to Xarelto.

Coverage Options Under Medicare Part D

Medicare Part D provides coverage for prescription drugs through private insurance companies that contract with Medicare. There are 21 Medicare Part D plans in the Omaha, Lincoln, and Council metro areas. These plans are designed to offer affordable access to a wide range of medications, including Xarelto. As of the writing of this article (January 2024), all 21 Medicare Part D plans pay for Xarelto. However, it’s important to note that not all Part D plans cover every prescription drug.

These plans are designed to offer affordable access to a wide range of medications, including Xarelto. As of the writing of this article (January 2024), all 21 Medicare Part D plans pay for Xarelto. However, it’s important to note that not all Part D plans cover every prescription drug.

Each Medicare Part D plan has a formulary, which is a list of covered drugs. The formulary is divided into different tiers, each with a different cost-sharing structure. Xarelto may be included in the formulary, but its placement within the tiers can affect how much you must pay out of your pocket.

Typically, Part D plans place drugs in different tiers based on their cost and how they compare to other medications in terms of safety and effectiveness. The lower the tier, the lower your out-of-pocket costs will be. It’s worth noting that the formulary and tier structure can vary between different Part D plans, so reviewing your plan’s specific details is essential to determine if Xarelto is covered and at what cost.

How to Determine if Xarelto is Covered Under Your Medicare Part D Plan

How to Determine if Xarelto is Covered Under Your Medicare Part D Plan

You have a few options to determine if Xarelto is covered under your specific Medicare Part D plan. The first step is to review the plan’s formulary. You can usually find this information on the plan’s website or request a copy of the formulary from the insurance company.

When reviewing the formulary, look for Xarelto or its generic equivalent, rivaroxaban. Note the tier in which it is placed and the associated cost-sharing requirements. Remember that formularies can change from year to year, so reviewing the most up-to-date information is essential.

Another helpful resource is the Medicare Plan Finder tool the Centers for Medicare & Medicaid Services (CMS) provides. This online tool allows you to enter your zip code, current medications, and dosage information to compare different Part D plans in your area. The tool will provide a list of plans and estimated costs. You will learn whether Xarelto is covered and the monthly costs.

If you prefer a more personalized approach, contact the insurance company directly and speak with a representative. They can provide detailed information about your plan’s coverage for Xarelto, including any prior authorization requirements or restrictions.

We Can Help Unlock Your Part B Benefits

Like Medicare, Omaha Insurance Solutions uses a plan finder tool that reviews all the Part D plans, formularies, and prices. The tool shows the various plans, the drug tiers, the medication cost before the Gap (Donut Hole) and in the Gap (Donut Hole), and the total overall cost combining copays and premiums together. You will have a total annual cost for each plan, so you can compare. We also point out the plan’s Medicare star rating.

We can filter the Part D information in many ways so you can look at the data as it applies to you. Our service is free when you are a client. We do this every year during the Annual Election Period for our clients to ensure they are on the best plan for their medication needs and budget.

Researching and understanding your plan’s coverage for all your medications, including Xarelto, can help you make informed decisions about your healthcare and potentially save you money. But what should you do if your Part D plan does not cover Xarelto? Let’s explore the steps you can take in such a situation.

Steps to take if your plan does not cover Xarelto

If your Medicare Part D plan does not cover Xarelto, don’t panic. You can take several steps to explore alternative options and potentially lower your out-of-pocket costs.

1. Speak with your healthcare provider: Your healthcare provider can help you explore alternative medications covered by your plan or suggest other strategies to manage your condition effectively.

2. Request a formulary exception: Sometimes, your healthcare provider can submit a request to the insurance company for a formulary exception. This request outlines why Xarelto is medically necessary for you and provides supporting documentation. If the exception is approved, the insurance company may cover Xarelto, even if it’s not on the formulary.

3. Consider therapeutic alternatives: Your Part D plan may cover alternative medications within the same class as Xarelto. These medications work similarly to Xarelto and may be suitable for your condition. Your healthcare provider can guide you in exploring these alternatives.

4. Explore patient assistance programs: Pharmaceutical companies often offer patient assistance programs that provide financial assistance or free medication to individuals who meet specific eligibility criteria. Due to its high cost, these programs can be a valuable resource if you need help to afford Xarelto.

5. Review other Part D plans: If Xarelto is essential for your health and well-being, consider switching to a different one during the annual enrollment period, typically from October 15th to December 7th each year. By reviewing other plans, you may find one that covers Xarelto or offers more favorable coverage for your specific needs.

Remember, it’s crucial to consult with your healthcare provider and insurance company before changing your medication regimen or coverage. They can provide personalized guidance based on your specific health condition and insurance coverage.

Alternative options for accessing Xarelto at a lower cost

If Xarelto is not covered by your Medicare Part D plan or the out-of-pocket costs are prohibitively high, alternative options are available to access Xarelto at a lower cost.

If Xarelto is not covered by your Medicare Part D plan or the out-of-pocket costs are prohibitively high, alternative options are available to access Xarelto at a lower cost.

1. Generic alternatives: Generic versions of Xarelto, known as rivaroxaban, may be cheaper. Generic drugs contain the same active ingredients as their brand-name counterparts and are approved by the FDA as safe and effective. Speak with your healthcare provider and pharmacist to explore whether a generic alternative suits you.

2. Manufacturer discounts and coupons: The pharmaceutical manufacturer may offer discounts or coupons that can help reduce the cost of the medication. These savings programs are often available for eligible individuals who meet specific criteria. Check the manufacturer’s website or discuss these programs with your healthcare provider.

3. Medication assistance programs: Non-profit organizations and foundations may offer medication assistance programs that provide financial support or free medication to individuals in need. These programs often have specific eligibility criteria, so it’s important to research and understand the requirements before applying.

4. Pharmacy discount programs: Some pharmacies, including Xarelto, offer discount programs or savings cards to help lower prescription medication costs. These programs may provide discounts for individuals paying out-of-pocket or even those with insurance coverage.

It’s worth noting that while these alternative options can help reduce the cost of Xarelto, it’s important to discuss them with your healthcare provider and consider their recommendations. They can provide valuable insights based on your specific health condition and medication needs.

Tips for Maximizing your Medicare Part D coverage for Xarelto

To maximize your Medicare Part D coverage for Xarelto, consider the following tips:

1. Review your plan annually: Medicare Part D plans can change their formularies and coverage yearly. Take the time to review your plan’s coverage during the annual enrollment period with your agent to ensure Xarelto is still covered and assess any potential changes in cost-sharing requirements. From October 15th to December 7th, we work around the clock to ensure our clients’ medications are covered in their Part D or Medicare Advantage plan within their budget.

ensure Xarelto is still covered and assess any potential changes in cost-sharing requirements. From October 15th to December 7th, we work around the clock to ensure our clients’ medications are covered in their Part D or Medicare Advantage plan within their budget.

2. Consider the total cost: When evaluating different Part D plans, Don’t solely focus on the monthly premium- this is a very common mistake. Consider the deductible, copayments, and coinsurance, as these factors can significantly impact your out-of-pocket costs for Xarelto.

Total Annual Cost! Not just copays, or t just monthly premiums. Not just the cost outside the donut hole. It is the total annual cost you pay.

3. Utilize preferred pharmacies: Some Part D plans have preferred pharmacy networks to access medications at lower copayments. Check if your plan has a preferred pharmacy network, and consider utilizing these pharmacies to reduce your medication costs. I have had clients save hundreds and

4. Explore mail-order options: Mail-order pharmacies often offer discounted prices for prescription medications, including Xarelto. If your plan allows for mail-order prescriptions, it may be worth considering this option to save on your medication costs.

By staying proactive and informed, you can maximize your Medicare Part D coverage and ensure affordable access to Xarelto.

Common Misconceptions about Medicare Part D Coverage for Xarelto

There are several common misconceptions about Medicare Part D coverage for Xarelto that are important to address:

There are several common misconceptions about Medicare Part D coverage for Xarelto that are important to address:

1. All Part D plans cover Xarelto: Not all Part D plans cover Xarelto, and its coverage can vary depending on the plan. Review your specific plan’s formulary to determine if Xarelto is covered and at what cost is essential.

2. Coverage is the same across all Part D plans: Xarelto’s coverage and cost-sharing requirements can vary between different Part D plans. It’s crucial to compare the formularies and associated costs of various plans to find one that suits your needs.

3. Once covered, Xarelto will always be covered: Formularies can change annually, and a medication covered in the past may not be covered in the future. Reviewing your plan’s formulary annually during the annual enrollment period is vital to ensure Xarelto is still covered.

This Medicare mistake is the bane of my existence. Some clients do not take the annual review period seriously. They do not send us an updated list of medications. They do not talk with us, and when January comes—and it is too late—they call because a particular medication is not covered or the cost is significantly higher than the previous year.

4. Generic alternatives are always covered: While generic alternatives are often less expensive, they may not be covered by all Part D plans. Reviewing your plan’s formulary is crucial to determine if the generic version of Xarelto is covered.

By dispelling these misconceptions, you can approach your Medicare Part D coverage for Xarelto with a clear understanding of what to expect and how to navigate the system’s complexities.

Resources and Assistance Programs for Xarelto Users

If you need assistance accessing Xarelto or managing the cost of the medication, several resources and assistance programs can provide support:

1. Extra Help/Low-Income Subsidy: The Extra Help program is a federal program that helps individuals with limited income and resources pay for their Medicare prescription drug costs. Eligible individuals can receive assistance with premiums, deductibles, and copayments. To determine if you qualify for Extra Help, contact the Social Security Administration or visit their website.

2. Patient Assistance Programs (PAPs): Pharmaceutical manufacturers often offer patient assistance programs that provide free or low-cost medications to individuals who meet specific eligibility criteria. These programs can be a valuable resource for individuals who cannot afford their medications, including Xarelto. Check the manufacturer’s website or discuss these programs with your healthcare provider.

3. State Pharmaceutical Assistance Programs (SPAPs): Some states have their own pharmaceutical assistance programs that provide financial assistance or low-cost medications to eligible individuals. These programs may have specific eligibility criteria and income limits, so it’s important to research the programs available in your state. Nebraska and Iowa do not have these types of programs.

4. Non-profit organizations and foundations: Various non-profit organizations and foundations provide financial assistance or free medication programs for individuals in need. These programs often have specific eligibility criteria and may focus on particular medical conditions. Research and reach out to relevant organizations to explore potential assistance options.

By leveraging these resources and programs, you can access the support you need to afford Xarelto and manage your health effectively.

Conclusion: Making Informed Decisions about Medicare Part D Coverage for Xarelto

Understanding the complexities of Medicare Part D coverage for Xarelto is essential for individuals who rely on this medication to manage their health conditions effectively. By delving into the details of coverage

Christopher J. Grimmond

options, determining if Xarelto is covered by your specific plan, exploring alternative options, and maximizing your Part D coverage, you can make informed decisions about your healthcare.

Remember to consult with your healthcare provider and insurance agent professional throughout the process to ensure you make decisions that align with your specific health needs. By staying proactive and informed, you can unlock the benefits of Medicare Part D and access the necessary medications, such as Xarelto, at an affordable cost. Give us a call at Omaha Insurance Solutions at 402-614-3389, and we will help unlock the benefits of Medicare Part D for you.

Are you looking for comprehensive information on Medicare coverage for Ozempic? Look no further! In this article, we’ll provide everything you need to know about this medication and how Medicare covers it.

Are you looking for comprehensive information on Medicare coverage for Ozempic? Look no further! In this article, we’ll provide everything you need to know about this medication and how Medicare covers it.

Ozempic is a popular prescription medication used to treat type 2 diabetes. It belongs to a class of drugs called GLP-1 receptor agonists, which help lower blood sugar levels and improve overall glycemic control in individuals with diabetes. However, understanding how Medicare covers this medication can sometimes be confusing.

Whether you’re already enrolled in Medicare or planning to do so, it’s crucial to understand the coverage options available for Ozempic clearly. This knowledge can help you make informed decisions about your healthcare and ensure you receive the treatment you need while minimizing out-of-pocket costs.

In this article, we’ll dive into various aspects of Medicare coverage for Ozempic, including the different parts of Medicare, potential costs, coverage criteria, and more. So, if you’re ready to learn about Medicare coverage for Ozempic, let’s get started!

What is Ozempic?

Ozempic is a medication used to treat type 2 diabetes in the class of drugs called GLP-1 receptor agonists, which help lower blood sugar levels. This medication is administered once weekly via injection, making it a convenient option for those managing diabetes. Ozempic is effective in reducing A1C levels and promoting weight loss in patients.

-

How Does Ozempic Work?

Ozempic works by mimicking the action of a naturally occurring hormone called glucagon-like peptide-1 (GLP-1) in the body. GLP-1 helps regulate blood sugar levels by stimulating insulin release, slowing down digestion, and reducing appetite. By activating GLP-1 receptors, Ozempic helps lower blood sugar levels, decrease appetite, and promote weight loss.

body. GLP-1 helps regulate blood sugar levels by stimulating insulin release, slowing down digestion, and reducing appetite. By activating GLP-1 receptors, Ozempic helps lower blood sugar levels, decrease appetite, and promote weight loss.

-

Who Can Benefit from Ozempic?

Ozempic is primarily prescribed to individuals with type 2 diabetes who have not achieved adequate glycemic control through lifestyle changes, such as diet and exercise, or oral diabetes medications alone. It is typically used as an adjunct to diet and exercise to improve blood sugar control.

Like any medication, Ozempic may have potential side effects. Common side effects may include nausea, vomiting, diarrhea, and constipation. These side effects are usually mild and tend to improve over time. However, discussing any concerns or persistent side effects with your healthcare provider is essential.

The Importance of Medicare Coverage for Ozempic

The Importance of Medicare Coverage for Ozempic

Understanding Medicare coverage for Ozempic is crucial, especially for individuals with type 2 diabetes who rely on this medication for their health and well-being. Medicare is a federal health insurance program that provides coverage for eligible individuals aged 65 and older, as well as individuals with specific disabilities. Having Medicare coverage for Ozempic can significantly reduce out-of-pocket costs for an expensive medication and ensure access to this essential treatment. According to CMS (Center for Medicare & Medicaid Services), over 459,000 Medicare beneficiaries were on Ozempic, costing CMS over $2.6 billion in 2021.

Understanding Medicare Part D Prescription Drug Coverage

Medicare Part D is the prescription drug coverage portion of Medicare. It is an optional benefit that helps cover the cost of prescription medications, including Ozempic. To receive Medicare Part D coverage, individuals must be enroll in a standalone prescription drug plan (PDP) or a Medicare Advantage plan (Part C) that includes prescription drug coverage.

Private insurance companies approved by Medicare offer Medicare Part D plans. These plans have formularies, which are lists of covered medications. Ozempic is typically included in the formularies of most Medicare Part D plans, but the specific coverage details may vary. It’s essential to review the formulary of the plan you’re considering to ensure Ozempic is covered and to understand any associated costs.

Medicare Part D in the Omaha Metro

There are 21 Medicare Part D prescription drug plans among seven private insurance companies in the Omaha, Lincoln, and Council Bluffs areas. Seventeen Part D prescription drug plans cover Ozempic. Four do not currently include Ozempic on the formulary. If you are enrolled in those plans, you will have to work with the plan and your doctor for an exception.

There are 21 Medicare Part D prescription drug plans among seven private insurance companies in the Omaha, Lincoln, and Council Bluffs areas. Seventeen Part D prescription drug plans cover Ozempic. Four do not currently include Ozempic on the formulary. If you are enrolled in those plans, you will have to work with the plan and your doctor for an exception.

The plan cost of Ozempic ranges from approximately $800-$950 per month. This amount is used to calculate the levels of cost sharing between the plan and you. This cost-sharing also includes any other medications you are taking. The total will determine how quickly you go from the initial phase, where your Ozempic may cost only $11 to $47 for a month’s supply, to the Gap, when Ozempic may jump to $150–$250, depending upon the plan, excluding your monthly premium for the plan itself.

Medicare Part C or Medicare Advantage in the Omaha Metro

Medicare Part C or Medicare Advantage in the Omaha Metro

There are 22 Medicare Advantage/Part C plans with prescription drug coverage among six private insurance companies in the Omaha, Lincoln, and Council Bluffs areas. All 21 Advantage plans list Ozempic on their formulary. The plan cost of Ozempic ranges from approximately $890 to $950 per month. This amount is used to calculate the levels of cost sharing between the plan and you. This cost-sharing also includes any other medications you are taking. The total will determine how quickly you go from the initial phase, where your Ozempic may cost only $47 for a month’s supply, to the Gap, when Ozempic may jump to $225–$295, depending upon the plan, excluding your monthly premium for the plan itself if it is not zero.

Eligibility Criteria for Medicare Coverage of Ozempic

To be eligible for Medicare coverage of Ozempic, you must be enrolled in Medicare Part D or a Medicare Advantage plan that includes prescription drug coverage. Individuals eligible for Medicare Part A and/or Part B are generally eligible for Medicare Part D.

To be eligible for Medicare coverage of Ozempic, you must be enrolled in Medicare Part D or a Medicare Advantage plan that includes prescription drug coverage. Individuals eligible for Medicare Part A and/or Part B are generally eligible for Medicare Part D.

Additionally, Medicare Part D plans may have their own eligibility criteria, such as residence in a specific service area or specific medical conditions. Reviewing the eligibility requirements of the Part D plans in your area is essential to ensure you meet the criteria.

Generally, once your doctor prescripts Ozempic within the standard amounts, the plan will cover Ozempic if it is on the formulary. If it is not on the formulary, you will need to apply for an exception.

Steps to Obtain Medicare Coverage for Ozempic

To obtain Medicare coverage for Ozempic, follow these general steps:

- Enroll in Medicare Part A and/or Part B if you haven’t already done so.

- Decide whether to enroll in a standalone Medicare Part D plan or a Medicare Advantage plan with prescription drug coverage.

- Research and compare Part D plans available in your area to find one that covers Ozempic and meets your healthcare needs.

- Enroll in the Part D plan of your choice during the initial or annual open enrollment period.

- Once enrolled, work with your healthcare provider to obtain a prescription for Ozempic.

- Take your prescription to a pharmacy in-network with your Part D plan and fill your prescription.

It’s important to note that the specific steps and requirements may vary depending on your location and the Part D plan you choose. Consult with Medicare resources or a licensed insurance agent for personalized guidance.

Medicare Coverage Limitations for Ozempic

While Medicare Part D covers Ozempic, certain limitations and cost-sharing requirements may exist. These limitations can include:

- Deductible: Part D plans may have an annual deductible that must be met before coverage begins. The deductible amount varies by plan. The maximum deductible for 2024 is $545. Twelve Part D plans in

our area out of 21 have a $545 deductible. Three Part D plans have a zero deductible.

our area out of 21 have a $545 deductible. Three Part D plans have a zero deductible. - Copayments or Coinsurance: After meeting the deductible, you may be responsible for copayments or coinsurance for each prescription. The amount will depend on the specific plan and formulary tier Ozempic falls under.

- Quantity Limits: Some Part D plans may impose quantity limits on Ozempic, meaning they will only cover a certain amount per prescription or within a specific time frame.

- Prior Authorization: Certain Part D plans may require prior authorization before covering Ozempic. This means that your healthcare provider will need to provide additional information to the plan to demonstrate medical necessity.

Reviewing the details of your chosen Part D plan to understand any limitations and cost-sharing requirements associated with Ozempic is crucial.

Alternative Options for Obtaining Ozempic

In addition to Medicare Part D coverage, there are alternative options for obtaining Ozempic. These options include:

- Manufacturer Assistance Programs: The manufacturer of Ozempic may offer assistance programs to individuals who meet certain eligibility criteria. These programs can provide financial assistance or free medication to eligible individuals.

- Pharmaceutical Discount Cards: Various pharmaceutical discount cards are available that can help reduce the cost of medications, including Ozempic. These cards are typically free and can be used in addition to Medicare Part D coverage.

- State Pharmaceutical Assistance Programs (SPAPs): Some states offer SPAPs that provide additional prescription drug coverage or financial assistance to eligible individuals. These programs can help lower the cost of Ozempic for those who qualify. Nebraska and Iowa do not have these programs.

- EXTRA HELP is a federal program for those on Medicare to help with medication costs. Assistance depends upon income limits and asset levels.

It’s important to explore these alternative options to ensure you’re taking advantage of all available resources for obtaining Ozempic at an affordable cost.

Additional Resources for Understanding Medicare Coverage for Ozempic

Understanding the intricacies of Medicare coverage for Ozempic can be complex. Fortunately, there are additional resources available to help you navigate this process:

- Medicare.gov: The official Medicare website provides comprehensive information about Medicare coverage options, including Part D and prescription drug coverage. The website provides detailed information, plan comparisons, and enrollment resources.

- State Health Insurance Assistance Programs (SHIPs): Each state has SHIPs that offer free, personalized assistance to Medicare beneficiaries. These programs can guide Medicare coverage options, including Part D, and help you understand how Ozempic is covered in your specific state.

- Licensed Insurance Agents: Working with a licensed insurance agent specializing in Medicare can provide valuable guidance and support. These professionals can help you navigate your area’s various Part D plans and assist with enrollment.

The Bottom Line On Ozempic Medicare Coverage

Christopher Grimmond

Medicare coverage for Ozempic is an important consideration for individuals with type 2 diabetes. Understanding how Medicare Part D works and the potential costs associated with obtaining Ozempic can help ensure you have access to this medication while minimizing out-of-pocket expenses. By utilizing the resources available and exploring alternative options, you can make informed decisions about your healthcare and receive the necessary coverage for Ozempic.

We are a local and independent Medicare insurance agency. Let us find the plan that covers your medications within your budget. We cost you nothing. We charge you nothing. We’re FREE. Call us at 402-614-3389 to speak with a licensed insurance agent professional with over 20 years of insurance experience and over 2,000 Medicare insurance clients. We will get it done right.

The Power of Negotiation Enables Medicare to Lower Drug Prices

In today’s healthcare landscape, the soaring cost of prescription drugs has become a critical concern for millions of Americans. As Medicare beneficiaries struggle with skyrocketing medication prices, the power to negotiate Medicare drug prices emerges as a potential solution.

With over 65 million enrollees, Medicare has significant purchasing power. However, unlike private insurers, Medicare is legally prohibited from directly negotiating drug prices with pharmaceutical companies. This restriction has prevented the program from achieving lower prices for its beneficiaries.

But what if Medicare could negotiate directly? What impact would it have on drug costs?

Empowering Medicare to negotiate drug prices may unlock savings all around, ensuring seniors receive affordable access to the medications they need. Or it may not. Let’s explore the government’s attempt to make Medicare drug prices more affordable through negotiations.

The Inflation Reduction Act of 2022

Medicare, the federal health insurance program for individuals aged 65 and older, is crucial in providing affordable healthcare to millions of Americans. With over 65 million enrollees, Medicare has substantial purchasing power. However, when negotiating drug prices, Medicare cannot negotiate directly with pharmaceutical companies.

healthcare to millions of Americans. With over 65 million enrollees, Medicare has substantial purchasing power. However, when negotiating drug prices, Medicare cannot negotiate directly with pharmaceutical companies.

Medicare is divided into parts, including Part A, which covers hospital insurance, and Part B, which covers medical insurance. Part D, prescription drug coverage, is the focus of this discussion. Medicare Part D provides beneficiaries access to a wide range of prescription medications, but the prices for some of these drugs are often exorbitant. The inability to negotiate directly with pharmaceutical companies has limited Medicare’s ability to control drug costs.

President Biden signed the Inflation Reduction Act of 2022 into law on August 16, 2022. One of the provisions of the law was to lower prescription drug costs for those on Medicare. The law gives the federal government limited power to negotiate drug prices for the costliest Medicare medications.

Non-Interference Clause Changed To Interference

The power to negotiate drug prices for Medicare Part D is a significant policy change. When the Medicare Part D program was created in 2004, the Health & Human Services Secretary was prohibited from interfering with negotiations between drug manufacturers, pharmacies, and prescription drug plan sponsors. This was the agreement at the time of Part D’s creation. It was referred to as the “Part D non-interference clause.”

A provision in the Inflation Reduction Act grants an exception to the non-interference clause. The law permits the HHS Secretary to directly negotiate with pharmaceutical companies on behalf of Medicare and the sponsored plans for a limited number of drugs with only single-source and non-generic brands starting in 2026 for Part D and 2028 for Part B medications.

The schedule for the negotiations is set, but the implementation of the changes is not scheduled to take effect until 2026. That is when the first set of selected drugs with newly negotiated prices covered under Part D will be available.

Price Controls & Punishing Penalties for Pharmaceutical Companies

Another policy change is that drug companies will be penalized for raising prices higher than the current inflation rate. They will be required to pay Medicare rebates for drug prices exceeding the consumer price index (CPI-U). The penalties will be for those most expensive drugs that HHS identifies. This is an entirely new power for the HHS Secretary. The Part D inflation rebate provision takes effect in 2022, so prices and inflation will be measured from that point. The rebate penalty will start in 2023.

$35 Insulin on Medicare

Diabetes is a growing problem in the U.S., including among Medicare beneficiaries. Insulin costs among this population have been staggering. In 2023, as part of the Inflation Reduction Act, insulin offered under Part D is set at $35 during the deductible, the initial phase, and even during the Medicare gap (donut hole). A prescription plan is not required to offer all insulins, but the ones they do must not exceed $35, and some are even $11.

$2,000 Out-of-Pocket Cap on Part D Prescriptions

The Medicare provision of the Inflation Reduction Act caps out-of-pocket spending for Medicare Part D beneficiaries at $2,000 in 2025 for each individual, excluding premiums. The 2024 provision of the law eliminates the 5% catastrophic Part D phase, effectively capping medication costs at $3,250 for 2024.

August 29, 2023: The HHS secretary announced the first list of ten medications for Medicare drug price negotiations.

- Eliquis-Bristol-Myers Squibb-a blood thinner to prevent blood clotting to reduce the risk of stroke

- Xarelto—Johnson & Johnson–a blood thinner to prevent blood clotting to reduce the risk of stroke

- Januvia—Merck–a diabetes drug to lower blood sugar for Type 2 diabetes

- Jardiance—Boehringer Ingelheim–a diabetes drug to lower blood sugar for Type 2 diabetes

- Enbrel—Amgen–a rheumatoid arthritis drug

- Imbruvica—Abbie–a drug for blood cancers

- Farxiga—AstraZeneca–a drug for Type 2diabetes, heart failure, and chronic kidney disease

- Entresto—Novartis–a heart failure drug

- Stelara—Janssen–a drug for psoriasis & Crohn’s disease

- Fiasp & NovoLog—Novo Nordisk—insulins for diabetes

According to CMS (Center for Medicare & Medicaid Services), these ten drugs were selected because they account for $50.5 billion, or 20% of Medicare Part D spending from June 1, 2022 to May 31st. They are very commonly used medications by the Medicare population.

My Experience As An Insurance Professional

I can attest to this fact after the Annual Election Period for 2023. We ran hundreds of Part D prescription drug plans for clients. These medications come up over and over again, and they are the cause of incredibly high copay totals for clients.

For those on Medicare, nearly 1 in 10 have heart conditions that put them at risk of blood clots. I see Eliquis and Xarelto were on many clients’ medication lists this year. Diabetes affects 28%, so Januvia, Jardiance, and NovoLog appear repeatedly. Some of my clients should be on Enbrel for rheumatoid arthritis, but even with Medicare insurance, the cost is beyond their reach.

Medicare Drug Price Negotiations May Be an Empty Jester

The law is not without its challengers. Several pharmaceutical companies are suing the federal government for its overreach into their business. The government is attacking their right to free speech but also threatening industry and individual businesses with extinction if they do not comply with the “negotiated” terms of the “agreement.”

The law is not without its challengers. Several pharmaceutical companies are suing the federal government for its overreach into their business. The government is attacking their right to free speech but also threatening industry and individual businesses with extinction if they do not comply with the “negotiated” terms of the “agreement.”

The U.S. Chamber of Commerce sought an injunction to halt preliminary negotiations on Oct 1, 2023, the day the drug companies were required to sign an agreement to participate in the negotiations. A federal judge, U.S. District Judge Michael Newman, in Dayton, Ohio, ruled on Sept 29, 2023, that negotiation could go forward.

Johnson & Johnson owns the drugmaker Janssen. In a lawsuit filed July 2023 in U.S. District Court in Trenton, N.J., Johnson & Johnson claimed Medicare drug price negotiations are unconstitutional. The situation leaves its company, Janssen, with no choice if it refuses to negotiate on Stelar because it must withdraw all drugs from Medicare and Medicaid, which is 40% of the U.S. healthcare market. “It is akin to the government taking your car on terms that you would never voluntarily accept and threatening to take your house if you do not ‘agree’ that the taking was ‘fair,’” the company said.

The myriad legal challenges could significantly delay or completely overturn the law’s implementation.

Innovation & Markets May Render the Law Meaningless

All of this activity may end up being an exercise in political theater. Politicians appear to care about the average citizen on Medicare, and the insurance companies keep making money from high-priced medications.

All of this activity may end up being an exercise in political theater. Politicians appear to care about the average citizen on Medicare, and the insurance companies keep making money from high-priced medications.

The pharmaceutical behemoth, Merck, will likely lose its exclusivity in 2026 on its medication, Januvia, one of the first ten drugs up for negotiation. If that happens, most of the business will go to cheaper generic versions when the patent expires.

The same can be said for AstraZeneca’s Farxiga for Type 2 diabetics. AstraZeneca will lose its exclusive patent in 2026. Johnson & Johnson’s Xarelto, Novartis, and Entresto will lose exclusivity in 2027. Many of these drugs on the first list may come down significantly in price naturally through market forces, especially if the current schedule of drug negotiations is delayed through litigation. The desired effect will take place. Lower drug costs. The cause may not be government coercion but rather the effects of innovations and competition. The politicians, however, will take the bows if it works.

Eliquis, taken for blood thinning, will no longer be protected by its patent in 2028. Bristol-Myers Squibb and Pfizer’s revenue will decline, whether by government legislation or patents ending.

Competition is also eroding prices. AstraZeneca has Calquence, and Beigene has Brukinsa. Both are for blood cancer, which now competes directly against AbbVie’s Imbruvica.

Ultimately, the consumer may still benefit, but it may not be by the hands of the politicians who claim credit.

Help Is on the Way

Whether from government intervention or efficient capital markets and technological advances, medication prices, like microchips, computers, and flat-screen televisions, will go down. I remember when Celebrex was a high-dollar medication. Celecoxib, the generic, is now $5 or even zero on some plans. Then, there will be new medications that are better than the ones we use now, but if we want to use those newer, better medications, we will have to pay new, higher prices.

Every year during the Annual Election Period, we run the medications for our clients to ensure they have a reliable plan with the lowest possible overall costs, regardless of Medicare drug price negotiations. We look at all the moving parts: premium, deductible, gap.

Christopher J. Grimmond, MA, CFP

Call us at Omaha Insurance Solutions at 402-614-3389 to speak with a licensed insurance agent professional to make sure you have the plan that meets your needs and budget.

When I meet with prospective clients, I begin with a brief explanation of Medicare. Then move on to the hundreds of plans. Drugs are next. This is hard. Clients must lay down their cards; some hold a straight flush of costly medications.

The Inflation Reduction Act of 2022 is a long-awaited solution to improve Medicare drug plans and make Part D affordable for those on costly medications.

Inflation Reduction Act of 2022 Deals with Medicare Drug Changes

When Medicare Part D was first established, Medicare contracted with private plan sponsors to provide the prescription drug benefit. The private insurance company created the Part D Prescription Drug Plans (PDP), sold the PDPs, and managed the PDPs. Each company negotiated separately with the pharmaceutical companies the price of the medications and which medications would be included on the plan formularies–the list of authorized drugs.

The insurance companies had the leverage of their brand and how many customers they would bring to the pharmaceutical companies. They were also competing with the other insurance companies to get more medications at the lowest cost. The pharmaceutical companies, of course, were trying to maximize their revenues and profits.

Ideally, it was hoped that the competition and freedom of the market would keep prices low. However, patent laws create a temporary monopoly for pharmaceutical companies that develop these very effective and popular new drugs. The patent, and the consequent monopoly, benefit the nation and the world with the newest and best medications. Unfortunately, it is a substantial financial burden for those who need the medication.

The Inflation Reduction Act Creates Leverage for Medicare

When Part D was created in 2004, a law was established known as “non-interference.” Non-interference means that the Secretary of Health and Human Services (HHS) cannot negotiate drug pricing with pharmaceutical companies, pharmacies, and insurance companies. Instead, the prices would be determined exclusively between the insurance companies, pharmaceutical companies, and pharmacies competing amongst one another.

With the Inflation Reduction Act of 2022, Medicare changes the law. The Secretary of HHS is granted a narrow exception to the non-interference clause. The HHS Secretary can negotiate on behalf of the 84 million Medicare and 76 million Medicaid beneficiaries for the lowest prices for a very limited number of costly prescriptions. The category of medications is single-source brand-name drugs or biologics without generic or biosimilar competitors.

Inflation Reduction Act of 2022 Effects Medicare Change in 2026

The Drug Price Negotiation Program begins in 2026 and is limited to 10 Part D drugs. Another 15 Part D drugs will be added in 2027, 15 Part D in 20228, and 20 Part in 2029. The HHS Secretary will select the drugs from among the 50 highest total cost Part D medications.

The timeline for the negotiation process will span roughly two years. For those companies that do not comply, there is an excise tax. The tax penalty starts at 65% of the product sales in the U.S. and increases by 10% every quarter to a maximum of 95%. The other option is that company can remove all its medications from the Medicare and Medicaid market.

Is the CBO Accurate, Reliable, & Trustworthy?

The Congressional Budget Office (CBO) claims HHS Secretaries’ ability to negotiate prices with Part D producers will significantly reduce what Medicare spends over the next ten years. The CBO also claims that reducing the revenue to pharmaceutical companies will have little effect upon developing new and better drugs. These are all projections and opinions to support the policy change. There is no evidence.

Drug Manufacturers Are Penalized for Inflation

The Inflation Reduction Act of 2002 adds another Medicare change. The Act requires drug manufacturers to pay a rebate to Medicare if prices for single-source drugs covered under Medicare Part B and nearly all covered frugs under part D increase faster than the rate of inflation reflected by the Consumer Price Index (CPI). The rebate dollars will be deposited in the Medicare Supplementary Medical Insurance (SMI) trust fund.

Cap Out-of-Pocket Part D Spending

Medicare Part D currently provides catastrophic coverage for high out-of-pocket drug costs. Still, there is no limit on the total amount beneficiaries pay out of pocket each year. Under the current design, Part D enrollees qualify for catastrophic coverage when the amount that they pay out of pocket plus the value of the manufacturer discount on the price of brand-name drugs in the coverage gap phase exceeds a certain threshold amount. Enrollees with drug costs high enough to exceed the catastrophic threshold must pay 5% of their total drug costs above the threshold until the end of the year. This can be huge.

The Inflation Reduction Act of 2022 amends Medicare’s design of Part D. For 2024, the law eliminates the 5% coinsurance requirement above the catastrophic coverage threshold, effectively capping out-of-pocket costs at approximately $3,250 that year.

The legislation adds a hard cap on out-of-pocket spending of $2,000 per person in 2025. How this will be funded, other than with savings, is still being determined.

Inflation Reduction Act of 2022 Puts Medicare Insulin at $35

Insulin is probably the most common high-dollar medication that burdens many Medicare beneficiaries. Most plans relieve several insulin products, beginning with the Trump Administration and now Biden.

Currently, Medicare beneficiaries can choose to enroll in a Part D plan participating in an Innovation Center model in which enhanced drug plans cover insulin products at a monthly copayment of $35 in the deductible, initial coverage, and coverage gap phases of the Part D benefit.

Participating plans do not have to cover all insulin products at the $35 monthly copayment amount, just one of each dosage form and insulin type (rapid-acting, short-acting, intermediate-acting, and long-acting).

While Medicare is incredible health insurance, Part D prescription drug plans are the weakness because of the light coverage for higher-end medication. The Inflation Reduction Act of 2022 helps Medicare better service citizens with more reasonably priced medications.

We can ensure you have the plan that best covers your prescription drug needs at the lowest possible cost.

Call 402-614-3389 to speak with an experienced and licensed agent and insurance professional.

Many people have heard of the Medicare Donut Hole, but even those on Medicare are not familiar with what the donut hole really means unless they fall into it.

When you are in the Medicare Donut Hole, you know it and quickly learn what it means.

Clients call me monthly asking, “What’s going on? My medication jumped from $45 to $145!” I say, “Oh, you’re probably in the Medicare Gap, or the more popular name is the ‘donut hole.”’ They ask, “What’s that?”