Prior authorization has arisen as an issue for Medicare Advantage Organizations (MAO)—insurance companies—and Medicaid–states. According to consumer claims, consumers are denied needed coverage unnecessarily. You can imagine the pain and hardship this causes. What if there was a Medicare prior authorization tool providers, insurance companies, and patients could use to communicate with one another?

Prior authorization has arisen as an issue for Medicare Advantage Organizations (MAO)—insurance companies—and Medicaid–states. According to consumer claims, consumers are denied needed coverage unnecessarily. You can imagine the pain and hardship this causes. What if there was a Medicare prior authorization tool providers, insurance companies, and patients could use to communicate with one another?

Congress recently conducted hearings on prior authorization denials, and the Department of Health & Human Services (DHHS), which is the ultimate supervising authority for Medicare (CMS) and Medicaid, issued a final rule that offers a partial solution to the problem.

DHHS initiated the creation of a Medicare prior authorization tool to speed up the process and reduce errors when it comes to prior authorizations for medically necessary treatments and procedures.

The DHHS Final Rule

The DHHS mandated the establishment of a standardized electronic platform for exchanging medical and billing information between payers (insurers and states—for Medicaid), providers, and consumers. All three will be able to see prior authorizations while in process in real-time and interact with one another.

Doctors will see their prior authorization submission as the payer (insurance company) processes the prior authorization. They will see if codes are incorrect or documentation is missing; if denied, doctors will see the reasons.

Payers will see additional information added and corrections made to the prior authorization requests in real-time. They can track the prior authorization because there is a timeline they all can see.

Payers can see the medical history and even similar prior authorizations approved or denied for the patient from the past.

Payers can better coordinate with other payers when other insurance companies may be involved.

Consumers can see that the doctor’s office is actually submitting the prior authorization and where the request is in the process rather than calling the provider to check-in.

DHHS aims to create a more efficient, responsive, and transparent system than the current process for prior authorization. This electronic platform will be for

- Medicare

- Medicaid

- Affordable Care Act (ACA) Marketplace

- CHIP (Children’s Health Insurance Program)

The platform is called Application Programming Interfaces (API). While it will be for government-sponsored health plans and not private insurance, like employer health plans, these types of institutional changes usually trickle down to the private sector eventually.

What’s on the Application Programming Interfaces (APIs)?

What’s on the Application Programming Interfaces (APIs)?

Providers, payers, and consumers will be able to look up:

- Medical items and services that require prior authorization.

- Required documentation for the plan to make a prior authorization decision.

- Current status of a prior authorization decision.

The API (Application Programming Interface) will be the Medicare prior authorization tool that allows providers and payers to communicate quickly and easily and consumers to monitor the process.

The prior authorization details available through the APIs will include:

- Prior authorization status

- Date of approval or denial of a prior authorization request

- Date or circumstance when the prior authorization ends.

- What items or medical services were approved

- Reason for denial: if denied

- Administrative and clinical information submitted by a provider.

This could also include information about past prior authorization decisions beneficial for a patient who is required to obtain prior authorization again for the same service when switching health plans.

Medicare Prior Authorization Timeframes

Currently, Medicare Advantage Plans can take up to 14 calendar days for a standard decision. Expedited decisions must be completed within 72 hours of the request for medical treatment.

With the final rule, prior authorization timeframes were shorted to 7 calendar days, and the same 72-hour rule was used to expedite prior authorization decisions.

Reasons For Denial

Reasons For Denial

The plans must explain the denial to the provider and patient through the APIs. This was not always done, especially if the denial was for miscoding or lack of supporting documentation.

Now, the patient can see the denial. They do not need to rely upon the doctor’s office to explain what the insurance company did or didn’t do, particularly if the provider’s back office did not provide adequate documentation. Everyone can see what the other one is doing or not doing.

Everyone can also see what can be done to appeal or overturn the denial.

Public Reporting of Medicare Prior Authorization Because of the Tool

Insurance companies will be required to report their denial ratios on their website. Consumers will be able to see how often insurance carriers deny prior authorizations and thus determine which Medicare Advantage plan or other government-sponsored programs to choose.

The hope is that Medicare Advantage Organizations (MAO) will be motivated to improve the prior authorization processes through education, better technology, and more efficient and robust systems.

robust systems.

The data required to be listed on the payer (insurance company) website will be:

- List of all items and services that require prior authorization.

- Percentage of standard and expedited prior authorization requests approved & denied (aggregated for all items and services)

- Percentage of standard prior authorization requests that were approved after appeal.

- Percentage of standard and expedited claims where decision timeframes were extended, followed by a request approval.

- Average and median timeframes between a prior authorization request and a decision for standard and expedited prior authorization requests.

Implementation January 2027

As with any government legislation and systemic changes, time is required. The DHHS final rule set January 2027 as the effective date for the proposed regulations.

Building a system as large as the API takes time to provide an effective and robust tool for the Medicare prior authorization process.

Bottom Line: Medicare Prior Authorization Tool

I find this awesome. Too many times, consumers are in the dark. All they know is they can’t get their treatment. They do not know the truth.

Is this something Medicare covers? Did the doctor’s office submit the request correctly, and did they fight to approve it? Is the insurance company being unreasonable? Can I do anything?

It is hard to bluff when everyone can see everyone else’s cards. Light is the best disinfectant for an infection.

People ask, what is the difference between Traditional Medicare (only Part A & Part B) and Medicare Advantage (or Part C)? Traditional Medicare does not require prior authorization.

People ask, what is the difference between Traditional Medicare (only Part A & Part B) and Medicare Advantage (or Part C)? Traditional Medicare does not require prior authorization.

Prior Authorization Contains Cost

Medicare Advantage is managed healthcare, similar to your health insurance policies under an employer health plan. A tool that managed healthcare uses is prior authorization to contain costs.

Utilization management first appeared in the 1960s after Medicare Part A was created. Once Medicare Part A was instituted, the number and length of hospital stays skyrocketed. To contain costs, President Johnson and Congress approved the practice of utilization reviews for hospital stays.

It Started with Utilization Reviews

Utilization reviews confirm the need for hospital treatment. Two doctors needed to concur on the diagnosis and the need for hospital treatment. The standard of treatment was called “reasonable and customary.” What would most doctors consider “reason and customary” for this diagnosis? Again, the purpose was to limit unnecessary hospital stays and cut costs.

The utilization review process, which gained traction in the health insurance industry, was primarily driven by the need to address issues of medical necessity, misuse, and overutilization of services. As a result, health plans began scrutinizing claims for medical necessity and the duration of hospital stays. In some cases, health plans even mandated that the physician certify the admission and subsequent days after the admission to curb costs.

Traditional Medicare Does Not Require Prior Authorization

Ironically, Traditional Medicare now requires almost no prior authorizations, limited to a few cases involving durable medical equipment. In contrast, Medicare Advantage, as a managed health care system, necessitates prior authorization for a majority of its procedures and tests, with the exception of routine doctor visits and common practices.

Under Traditional Medicare–with no prior authorization processes–the only mechanism to limit fraud, waste, and abuse of tax-payor-funded resources is the 800-number to which people may voluntarily report fraud, waste, and abuse.

Medicare Advantage Organizations are Scrutinized

Medicare Advantage Organizations (MAO) constantly monitor submissions to make sure the requests for treatment are “medically necessary” as defined by the CMS (Center for Medicare & Medicaid Services) regulations for standards of care.

To make sure the MAOs perform their mission correctly,

“CMS (Center for Medicare & Medicare Services) oversees an entity’s continued compliance with the requirements for an MA organization. If an entity no longer meets those requirements, CMS terminates the contract in accordance with procedures described in Subpart K at 42 CFR Part 422 .”

None of us would write a blank check for someone. We want guarantees that our money is spent correctly. Medicare Advantage Organizations (MAO) are no different. They also oversee that requests for reimbursement for treatments and procedures are within the standards of care that CMS authorizes.

An issue that has come up recently is: Are MAOs being too restrictive in their approvals of prior authorizations? After all, on the reverse side, the motivation for profits could motivate MAOs to restrict payments to keep revenue received from CMS for themselves.

Does Prior Authorization Hurt

Does Prior Authorization Hurt

Unfortunately, CMS does not currently require the MAOs to keep data on some aspects of prior authorization rejections. The two most recent studies are inadequate for giving a real idea.

Kaiser Family Foundation studied 35 million prior authorizations and found that less than 5 percent (or 2 million) were denied. It also noted that 82 percent of denials were overturned when appealed.

The Health & Human Services Office of Inspector General did a tiny study of less than 250 denials during one week in 2019. Among those denials, the OIG determined that 18 percent (or 33 cases) should not have been denied. The reasons for denials were not completely clear, though human error and lack of supporting documentation were the dominant reasons.

An objective and thorough study would be beneficial to dispel misunderstandings and false fears.

Prior Authorization Helps More Than Hurts

In my experience, prior authorizations that are denied do not require a formal appeal. The denial quite often is based on wrong codes, insufficient documentation, human error, and a lack of persistence on the part of the doctor’s back office.

The real question is not why Medicare Advantage has prior authorization. Instead, it is why Traditional Medicare does not protect patients and taxpayers from fraud, waste, and abuse with its own prior authorization protocols.

Are you considering enrolling in a Medicare Advantage plan? Before making a decision, it’s crucial to understand the coverage options and potential limitations. One common concern is whether Medicare Advantage plans can deny coverage because they require prior authorization.

Are you considering enrolling in a Medicare Advantage plan? Before making a decision, it’s crucial to understand the coverage options and potential limitations. One common concern is whether Medicare Advantage plans can deny coverage because they require prior authorization.

Medicare Advantage plans, or Medicare Part C, are offered by private insurance companies approved by Medicare. These plans provide all the benefits of Original Medicare (Parts A and B) and often include additional benefits such as prescription drug coverage and dental, vision, and hearing services.

We will delve into the specific circumstances in which a Medicare Advantage plan requires prior authorization and could potentially deny coverage, the appeals process for denied claims, and what steps you can take to ensure you receive the coverage you need. By understanding the ins and outs of Medicare Advantage plans, you can make an informed decision about your healthcare coverage. So, let’s unlock the truth together and navigate the world of Medicare Advantage plan prior authorization.

What is the Purpose of Prior Authorization?

Prior authorization (or Pre-Authorization) is a utilization management tool used to contain costs. It consists of a third party, usually employed by the insurance company, making determinations about a request for service. The third party, who may be a doctor, nurse, or non-medical staff, approves or denies a request based upon predetermined criteria.

• Is the service covered?

• Is it a duplicate?

• Does the request contain the proper codes and supporting documentation?

• Is the service “medically necessary” as defined by CMS’s standard of care?

The purpose of Medicare Advantage plans requiring prior authorization is to ensure that the medical procedures are necessary and that the payer (insurance company) and patient are not wasting money.

Health care involves a great deal of money. There are three primary interested parties: the patient, who wants to pay as little as possible, the doctor, who provides a service for a fee, and the insurance company, which protects the patient from overwhelming healthcare costs for a premium.

Each has different and conflicting interests. Each is making a cost-benefit analysis to determine if the activity is worth it.

The patient wants good care for minimal cost. The doctor wants to be paid as much as possible for skills and services rendered. The insurance company wants to provide protection at the lowest cost to itself to maximize profit. Each is attempting to protect its interests. The insurance company uses prior authorization to make sure the service is, in fact, medically necessary so it does not waste money on unnecessary services.

The tradeoff is that prior authorization creates a barrier that potentially delays care and adds to its cost. There is also the potential that needed healthcare is wrongly delayed or withheld.

Medicare Advantage Utilizes Prior Authorization

Like commercial health insurance your employer purchases for employees, Medicare Advantage requires prior authorization for a majority of procedures, tests, and treatments, especially the more costly treatments. If approval is not granted, the insurer does not pay. There is an appeal process; however, many do not utilize the appeal process.

Traditional Medicare does not employ utilization management tools like prior authorization except in a few instances. The lack of any supervision of the medical necessity of services and payments has resulted in some high-profile cases of fraud, waste, and abuse. The only mechanism to combat abuse is self-reporting, whistle blowers, and fraud hotlines.

Optimally, prior authorization deters patients from getting care that is not truly medically necessary, reducing costs for both insurers and enrollees. Prior authorization requirements, however, can also create hurdles and hassles for beneficiaries and their physicians and may limit access to both necessary as well as unnecessary care. It also adds the burden of expense to providers who pay staff to work with insurance companies through the prior authorization process.

Data suggests that Medicare Advantage members save an average of $1,965 per year in total health expenditures compared to fee-for-service Traditional Medicare. Medicare Advantage members have lower hospitalization rates and fewer readmissions than their Traditional Medicare counterparts.

Does Original Medicare Utilize Prior Authorization?

From its inception, Traditional Medicare (Original Medicare) has not used prior authorization. There was little, if any, oversight until the electric wheelchair scandal.

A Washington Post article published in August 2014 highlighted the massive fraud of Medicare’s resources. The article chronicled the sensational scams and trials of many Medicare swindlers. The outrageous theft of public funds and the massive fraud shamed CMS to amend its regulations to finally require pre-authorization for some “durable medical equipment,” i.e., electric wheelchairs.

Bureaucrats inside CMS admitted they knew how the wheelchair scheme worked as early as 1998. However, it was not until 15 years later that officials finally did enough to curb the practice significantly. Durable medical equipment—electric wheelchairs—is the only exception to the “reasonable and necessary” practice. They must be preapproved.

The Government Accountability Office (GAO) examined a prior authorization program that CMS ran in seven states in 20212. During the short duration of the program, Medicare saved $1.9 billion. The GAO recommended that CMS continue to study the subject and implement a prior authorization program for all of Original Medicare in its 2018 published study. CMS discontinued the program.

The Effect of Medicare Advantage Denials

The Effect of Medicare Advantage Denials

There may be severe consequences when a Medicare Advantage Organization (MAO) denies authorization for a procedure.

- Patient access to medical care is delayed or denied.

- Potentially, it results in the patient paying out of pocket for something Medicare should have covered.

- It causes an administrative burden for the patient and providers because they must devote resources to an appeal.

None of these have positive consequences and are a cause of frustration with Medicare Advantage for some.

How Common is Medicare Advantage Prior Authorization Denials?

The Kaiser Foundation examined CMS data from MAOs from 2021. They found that more than 35 million prior authorizations were submitted to Medicare Advantage insurers. Over 2 million prior authorization requests were fully or partially denied by the insurance companies.

The percentage of prior authorization requests and denials depends upon individual plans. They are not identical. Of the 2 million denials, some were partial denials, totaling 380,000.

Partial denials would be, for example, physical therapy sessions. The physician requests 10 sessions, but only 5 are granted. That leaves 1.6 million prior authorizations completely denied. The average for Medicare Advantage plans as a whole was less than 6 percent, with individual MAO falling slightly above or below that average.

How About Appeals of Prior Authorization Denials?

Each Medicare Advantage plan has an appeal process. Data from the same group revealed that only 11 percent (or 212,000) of appeals were made, including partially and fully denied requests. The insurance companies overturned 82 percent (or 173,000) of the appeals.

insurance companies overturned 82 percent (or 173,000) of the appeals.

The high number of repeals was cause for concern. Are Medicare beneficiaries being unjustly denied services? Are the insurance companies creating unfair obstacles to reduce costs?

The study’s data, however, do not describe in detail the causes of the denials. In general conversations with insurance carriers, the authors discovered that prior authorizations are denied for a number of common reasons.

- Incorrect coding and insufficient documentation

- Less intrusive or costly services were not first tried.

- The provider was not in the network

- Service is not covered

- Human error

All of these reasons may result in a denial of service, but the data does not identify the various causes, some of which are easily rectified upon review or appeal.

We have thousands of clients who call us when there are issues. I am amazed at how often the provider’s back office does not file the proper paperwork, use the correct codes, or include essential documentation such as X-rays or tests.

Then, when the pre-authorization is denied, the insurance company is blamed, and the subject is dropped. The back office is understaffed, doesn’t have the time, and doesn’t sufficiently understand the insurance company’s processes, so they cut their losses and move on to other cases. Sometimes, the provider moves on to the less costly treatment, knowing that it will be immediately approved.

How Many Are Denied Coverage Unnecessarily?

The Office of Inspector General (OIG) for the Department of Health & Human Services published a report in April 2022 regarding the denial of medically necessary services by some Medicare Advantage Organizations (MAO). The study discovered that MAOs denied services to Medicare beneficiaries on some MAO plans even though the prior authorization request did meet the standard for Medicare coverage rules.

The OIG study sample was taken from 15 of the largest MAOs during the week of June 1-7, 2019. The sample size was 500—250 prior authorizations and 250 denials of claims. Eventually, the number was reduced to 430 as the data was further sifted.

The OIG dug into the details of each of the 430 cases. In the course of the review of the cases, OIG found a conflict in the standards.

Conflict in Standards

CMS has its own guidance regarding the standard of care. The MAOs, however, have developed their own internal clinical criteria that go beyond Medicare coverage rules even though the case would pass CMS’s standards. In the past, CMS has left the MAOs to develop their own criteria where CMS is unclear. For example, a less intrusive or costly treatment may be required before a more expensive service is authorized by the MAO. Physical therapy may be more appropriate first before an MRI is prescribed.

Second, MAOs indicated that some prior authorization requests did not have enough documentation to support approval, yet OIG reviewers found that the existing beneficiary medical records were sufficient to support the medical necessity of the services.

On payment requests, the OIG found that the MAOs denied 18 percent of the cases that would have met the Medicare coverage and MAO billing rules. Most of these payment denials in the sample were caused by human error during manual claims processing reviews (e.g., overlooking a document) and system processing errors (e.g., the MAO’s system was not programmed or updated correctly).

In the end, OIG determined that 13 percent of the 250 prior authorization cases studied should not have been denied based upon CMS stands (or approximately 32 individuals).

How Many Denied Coverage Should Be Approved?

If we combine the two studies, Kaiser Foundation and Office of Inspector General for the Department of Health & Humana Services—we actually get an idea of who should have been approved.

The Kaiser Foundation consists of 35 million prior authorizations, with less than 2 million being denied, which is a 5 percent denial rate.

The OIG’s study discovered that only 13 percent of those denied should have been approved.

So, when we apply the average of 13% of wrongly denied prior authorization requests to the 2 million denials in the Kaiser study, that is approximately 260,000 individuals who should have been approved but were not out of 36 million prior authorization requests.

That means out of 36 million prior authorization requests, only 0.7 percent were wrongly denied coverage. In other words, 99.3 percent of prior authorizations are processed correctly.

I find that an incredibly high degree of accuracy.

Appeals and Reconsiderations for Denied Coverage

The appeals process for denied coverage with Medicare Advantage plans involves several levels, each with its own deadlines and requirements. Understanding these steps can help you navigate the process effectively and increase your chances of a successful appeal.

Redetermination

The first level of appeal is the “Redetermination” process. You must submit a written request to your Medicare Advantage plan within a specified timeframe, usually 60 days from the date of the denial letter. Include all relevant documentation and explain why you believe the service or procedure should be covered. The plan must review your appeal and provide a written decision within 30 days.

Reconsideration

If your appeal is denied at the redetermination level, you can proceed to the second level, known as a “Reconsideration.” This involves submitting a request to an independent review entity contracted by Medicare within 60 days of receiving the redetermination denial. The review entity will conduct a thorough review of your case, including any additional evidence you provide, and issue a written decision within 60 days.

Administrative Law Judge

If your appeal is still denied at the reconsideration level, you have the option to request a hearing before an administrative law judge (ALJ). This request must be made within 60 days of receiving the reconsideration denial. The ALJ will hold a hearing, either in person or by video conference, where you can present your case. The ALJ will issue a written decision within 90 days.

Medicare Appeals Council

If you are dissatisfied with the ALJ’s decision, you can further appeal to the Medicare Appeals Council. This request must be made within 60 days of receiving the ALJ’s decision. The council will review your case and issue a written decision.

Federal District Court

The final level of appeal is to seek judicial review in a federal district court. This step involves filing a lawsuit against the Medicare Advantage plan in a federal court. It’s important to consult with legal counsel if you reach this stage, as the process can be complex.

Bottom Line: Medicare Advantage Prior Authorization Is a Required Tool

No one writes a blank check. When money is being spent, there is oversight. When there is a lot of money from a lot of people, there will be a lot of accountability. The Medicare Advantage oversees that taxpayers’ and beneficiaries’ money is spent in accordance with the norms and procedures that CMS has laid down. Medicare Advantage requires prior authorization to protect resources and clients, but like any institution that is carrying out millions of actions among thousands of people, there are errors. The appeals process is supposed to remedy those errors, but in an imperfect world, not always.

Currently, no one has complete and adequate data to give an accurate idea of inappropriate Medicare Advantage denials, but the data and studies recently done show that the level of error is incredibly low.

Over the years, the process I use to introduce clients to Medicare and Medicare insurance has evolved. This evolution has been based on my personal and professional growth. The process has evolved chiefly because Medicare and insurance companies have evolved. Clients and their needs change and evolve as well. Paying for Medicare is one of those changes. So, how do Medicare payments work in 2024?

Over the years, the process I use to introduce clients to Medicare and Medicare insurance has evolved. This evolution has been based on my personal and professional growth. The process has evolved chiefly because Medicare and insurance companies have evolved. Clients and their needs change and evolve as well. Paying for Medicare is one of those changes. So, how do Medicare payments work in 2024?

Delayed Social Security Benefits

More clients retire or take Social Security Benefits at full retirement age, which is at least 66 and 10 months. (Next year, full Social Security Benefits will be at age 67 for everyone, or 67 for those born in 1960 or later.) Medicare eligibility, however, remains at 65.

Consequently, Medicare beneficiaries need a way to pay their Medicare Part B premium. In the past, the monthly Part B premium was deducted directly from a person’s Social Security check, but since most are delaying Social Security Benefits, you must pay a different way.

Medicare Payment Options for 2024

Medicare Payment Options for 2024

There are four ways to make your Medicare Part B premium payment for 2024.

- You can pay by check quarterly through the mail upon receipt of your bill for Part B from Social Security. The SSA only accepts checks for quarterly payments.

- Pay online from your checking account monthly with an EFT (electronic funds transfer).

- Pay online by credit card monthly.

- Pay by monthly deduction from your Social Security.

The place where your Medicare payments for 2024 occur is in your MyMedicare.gov online account.

At the end of an enrollment appointment, I ask clients how they wish to pay their Medicare Part B premium if they are not getting Social Security benefits. Most do not have a MyMedicare.gov account, so I set it up for them at the end of the meeting.

Online Medicare Payment for 2024 Instructions

Here is how to do it.

- Type mymedicare.gov in the address bar of your browser. You’ll arrive at the login site.

- Click the green “Create Account” button on the right.

- Fill out your protected health information (PHI). You must have a Medicare number to create an account.

- Create your personal login information: user name, password, and security questions. Press the complete button, and voila—you have a Medicare online account.

- Click the green button on the left of “Pay my premium.”

- Click the link “Set up reoccurring payments.”

- Fill out your banking information. You are done.

Your monthly 2024 Medicare Part B premium payments will be automatically deducted. With Medicare EasyPay, the SSA automatically deducts your monthly Medicare premiums from your checking or savings account. The statement includes the total SSA deductions for that month, which are itemized and broken down. Automatic deductions are generally made on the 20th of the month (or the next business day).

The Medicare Part B premium payment does not include any other payments, such as your Medicare Supplement, Medicare Advantage, or Part D premiums. Those are handled separately.

You do not need to do anything when the Part B premium increases. The withdrawal will be adjusted accordingly.

When you start your Social Security Benefits, the Part B premium will automatically switch to your Social Security check and be withdrawn, and SSA will stop deducting from your personal checking account.

No Forgiveness

No Forgiveness

Part B premium payment is critical. Over a decade with thousands of clients, I have only had a couple of clients forget to pay their Medicare Part B premium. The consequences were devastating. They lost their Medicare, resulting in penalties and lost health insurance. All medical bills came out of their pocket until they reactivated their Medicare insurance many months later. You cannot flip a switch and just turn Medicare back on. You must wait until General Medicare Enrollment Jan 1st-Mar 31st to reapply.

As more people postpone taking Social Security Benefits until well past 65, I have made it part of our enrollment meeting to help clients set up their MyMedicare.gov account to pay their Part B premium out of their checking account. Setting up Medicare EasyPay is not difficult, but when I do it for them, I know it is done and done correctly. There is nothing worse than a distressed phone call from a client who has lost Medicare.

Bottom Line: Don’t Miss Your Monthly Medicare Payment for 2024

Medicare insurance has many moving parts, and mistakes are unforgiven. At Omaha Insurance Solutions, we have helped thousands of clients over the years, so we know all that needs to be done for a

Christopher Grimmond

successful and happy retirement with Medicare health insurance. We will help you set up your 2024 Medicare Part B premium payments if you like. Give us a call at 402-614-3389 to speak with a professional and experienced licensed insurance agent about your Medicare needs. We’ll make sure nothing is missed or forgotten.

Finding effective solutions to manage weight loss can sometimes feel like searching for a needle in a haystack. But what if there was a medication that could help you on your journey? Enter Ozempic, a breakthrough drug making waves in the weight loss community. Does Medicare cover Ozempic for weight loss?

Finding effective solutions to manage weight loss can sometimes feel like searching for a needle in a haystack. But what if there was a medication that could help you on your journey? Enter Ozempic, a breakthrough drug making waves in the weight loss community. Does Medicare cover Ozempic for weight loss?

In this article, we will explore how Medicare may give you access to Ozempic, giving you the insights you need to make informed health decisions. We’ll also explore the eligibility criteria, coverage options, and potential costs. Whether you’re already enrolled in Medicare or considering it in the future, this information is invaluable for those seeking weight management solutions.

What is Ozempic?

Ozempic is a medication used to treat type 2 diabetes in the class of drugs called GLP-1 receptor agonists. As a GLP-1 receptor agonist, semaglutide enhances the effects of the naturally occurring hormone GLP-1, which helps lower blood sugar levels. This medication is administered once weekly via injection, making it a convenient option for those managing diabetes. Ozempic is effective in reducing A1C levels and promoting weight loss in patients.

A 0.25 or 0.5-milligram dose of Ozempic currently retails on the Novo Nordisk website for $935.77 without insurance. However, those with private or commercial insurance who are eligible for a prescription may pay as little as $25. Medicare Part D and Part D copays for Ozempic can be significantly higher, especially if you fall into the Gap (or Donut Hole).

How Does Ozempic Work?

Ozempic works by mimicking the action of a naturally occurring hormone called glucagon-like peptide-1 (GLP-1) in the body. GLP-1 helps regulate blood sugar levels by stimulating insulin release, slowing down digestion, and reducing appetite. By activating GLP-1 receptors, Ozempic helps lower blood sugar levels, decrease appetite, and promote weight loss.

Who Can Benefit from Ozempic?

Ozempic is primarily prescribed to individuals with type 2 diabetes who have not achieved adequate glycemic control through lifestyle changes, such as diet and exercise, or oral diabetes medications alone. It is typically used as an adjunct to diet and exercise to improve blood sugar control.

GLP-1 also impacts weight via two key mechanisms:

- Affects the hunger centers in the brain (specifically, in the hypothalamus), reducing hunger, appetite, and cravings

- Slows the rate of stomach emptying, effectively prolonging fullness and satiety after meals

The net result is decreased hunger, prolonged fullness, and, ultimately, weight loss.

The Benefits of Ozempic for Weight Loss

Ozempic has gained significant attention in the weight loss community due to its potential benefits. Studies have shown that Ozempic can lead to significant weight loss when used with a healthy diet and exercise. In fact, clinical trials have demonstrated that individuals using Ozempic experienced an average weight loss of 5-10% of their body weight over a 26-52 week period. This is a remarkable achievement, considering many individuals’ challenges when trying to lose weight.

In one large clinical trial sponsored by Novo Nordisk, 1,961 adults with excess weight or obesity who did not have diabetes were given 2.4 milligrams of semaglutide or a placebo once a week for 68 weeks, along with lifestyle intervention. Those who took semaglutide lost 14.9% of their body weight compared with 2.4% for those who took the placebo.

Understanding Medicare Coverage

Before we dive into the specifics of Medicare coverage for Ozempic, it’s important to have a basic understanding of how Medicare works.

Medicare is a federal health insurance program primarily designed for individuals aged 65 and older, as well as certain younger individuals with disabilities. It consists of different parts, including Part A (hospital insurance), Part B (medical insurance), Part C (Medicare Advantage), and Part D (prescription drug coverage).

Medicare covers a wide range of medical services and treatments, including prescription medications. However, coverage for prescription drugs can vary depending on the specific plan you have. Some plans may cover a broader range of medications, while others may have more limited coverage. Understanding your specific Medicare plan is essential to determining the coverage options available for Ozempic.

How Medicare Covers Ozempic for Weight Loss

How Medicare Covers Ozempic for Weight Loss

To determine if Ozempic is covered by Medicare for weight loss, you need to check whether it is included in your Medicare Part D plan’s formulary. A formulary is a list of prescription drugs covered by a specific Medicare plan. You can typically find this information in the plan’s drug formulary document, which is usually available on the plan’s website or by contacting customer service.

All 21 Medicare Part D prescription drug plans and all 30 Medicare Advantage plans cover Ozempic in the Omaha, Lincoln, and Council Bluffs areas. Depending on the plan, you may or may not have a drug deductible and then copays. Ozempic is usually a tier 3 medication with a hefty copay. Depending on your total medications, you may or may not go into the Gap (or Donut Hole).

If Ozempic is included in the formulary, it means that it is covered by your Medicare Part D or Part C plan. However, coverage may still be subject to certain conditions. The medication must be medically necessary for the prescribed purpose. Other factors include prior authorization or step therapy.

Prior authorization requires your healthcare provider to obtain approval from the Part D prescription drug plan before prescribing Ozempic, while step therapy may require you to try other medications before Ozempic is covered.

Review the specific coverage requirements outlined in your Medicare Part D plan to ensure you meet all the necessary criteria for Ozempic coverage. It is important to understand Medicare covers Ozempic for diabetic and pre-diabetic treatment. Medicare does not cover Ozempic for weight loss exclusively.

Why Medicare Does Not Cover Ozempic for Weight Loss

Medicare Part D prescription drug plans were created under the Busch Administration. The Medicare Prescription Drug, Improvement, and Modernization Act (MMA) of 2003 determined that Part D prescriptions could not cover medications for cosmetic or weight loss reasons. Thus, Ozempic is only covered by Medicare for type 2 diabetes. Ozempic is not covered by Medicare for weight loss.

Wegovy: An Alternative?

Wegovy is a brand-name version of the drug semaglutide, which is the medication Ozempic in a different dosage. The FDA approves Wegovy as a chronic weight management medication, not for type 2 diabetes, like Ozempic.

Medicare, however, does not cover Wegovy because the drug is for weight loss. Medicare does not cover weight loss medications even though obesity is intimately tied to diabetes and a cause of poor health.

How to Navigate the Medicare Coverage Process for Ozempic

Here are some suggestions for you to navigate the Medicare coverage process for Ozempic.

Here are some suggestions for you to navigate the Medicare coverage process for Ozempic.

Check the Formulary

Look for Ozempic in your plan’s formulary to determine if it is covered. Note any additional coverage requirements, such as prior authorization or step therapy.

Consult Your Healthcare Provider

Diabetes and pre-diabetes are usually related to obesity. Discuss your diabetes or pre-diabetes in relation to your weight loss goals with your healthcare provider. See if Ozempic is a suitable option for you. They can help guide you through the coverage process and provide any necessary documentation.

Prior Authorization or Step Therapy

If your plan requires prior authorization or step therapy for Ozempic, work with your healthcare provider to complete the necessary paperwork and submit it to Medicare for approval.

Those who are type 2 diabetic or pre-diabetic AND overweight may be able to get access to Ozempic for their healthcare needs, which secondarily includes weight loss.

Dangers of Ozempic

Ozempic, however, isn’t safe for everyone. According to the company, people with the following conditions should avoid using Ozempic:

- Pancreatitis

- Type 1 diabetes

- Under 18 years of age

- Pregnant or breastfeeding

- Diabetic retinopathy

- Problems with the pancreas or kidneys

- Family history of medullary thyroid carcinoma (MTC)

- Multiple Endocrine Neoplasia syndrome type 2 (MEN 2), an endocrine system condition

As with any prescription medication, you must consult your doctor or other qualified healthcare provider on whether this medication is safe for you and what dosage is appropriate.

Ozempic Side Effects and Health Risks

There are many side effects of taking Ozempic as a weight loss medication, including

- Gastrointestinal issues like nausea, vomiting, and diarrhea

- Constipation

- Stomach pain

- Headache

- Excessive burping

- Heartburn

- Fatigue

- Flatulence

- Gastroesophageal reflux disease

These most common side effects of Ozempic don’t tend to be dangerous and may dissipate as you grow used to the medication. However, there is potential for more serious adverse effects, such as:

- Vision problems

- Swelling in extremities

- Dizziness or fainting

- Reduced urination

- Rash

- Rapid heart rate

- Swelling of throat, tongue, mouth, face, or eyes

- Problems swallowing or breathing

- Fever

- Yellow eyes or skin

- Chronic upper stomach pain

Wegovy, another brand name for semaglutide, may also cause damage to the retina, suicidal ideation, gallstones, pancreatitis, and acute kidney damage.

Moreover, taking semaglutide can increase the chance of developing thyroid tumors, including medullary thyroid carcinoma. Speak with your doctor if you are experiencing any of the side effects listed above.

“Ozempic Face”

You may have heard about “Ozempic face” as a side effect of GLP-1 drugs, though the term is misleading because this can be a side effect of any GLP-1 drug or any other cause of rapid weight loss.

The rapid loss of fat in the face can cause:

- a hollowed look to the face

- changes in the size of the lips, cheeks, and chin

- wrinkles on the face

- sunken eyes

- sagging jowls around the jaw and neck.

If weight is lost more gradually, these changes may not be as noticeable. However, the faster pace of weight loss that occurs with GLP-1 drugs can make facial changes more obvious.

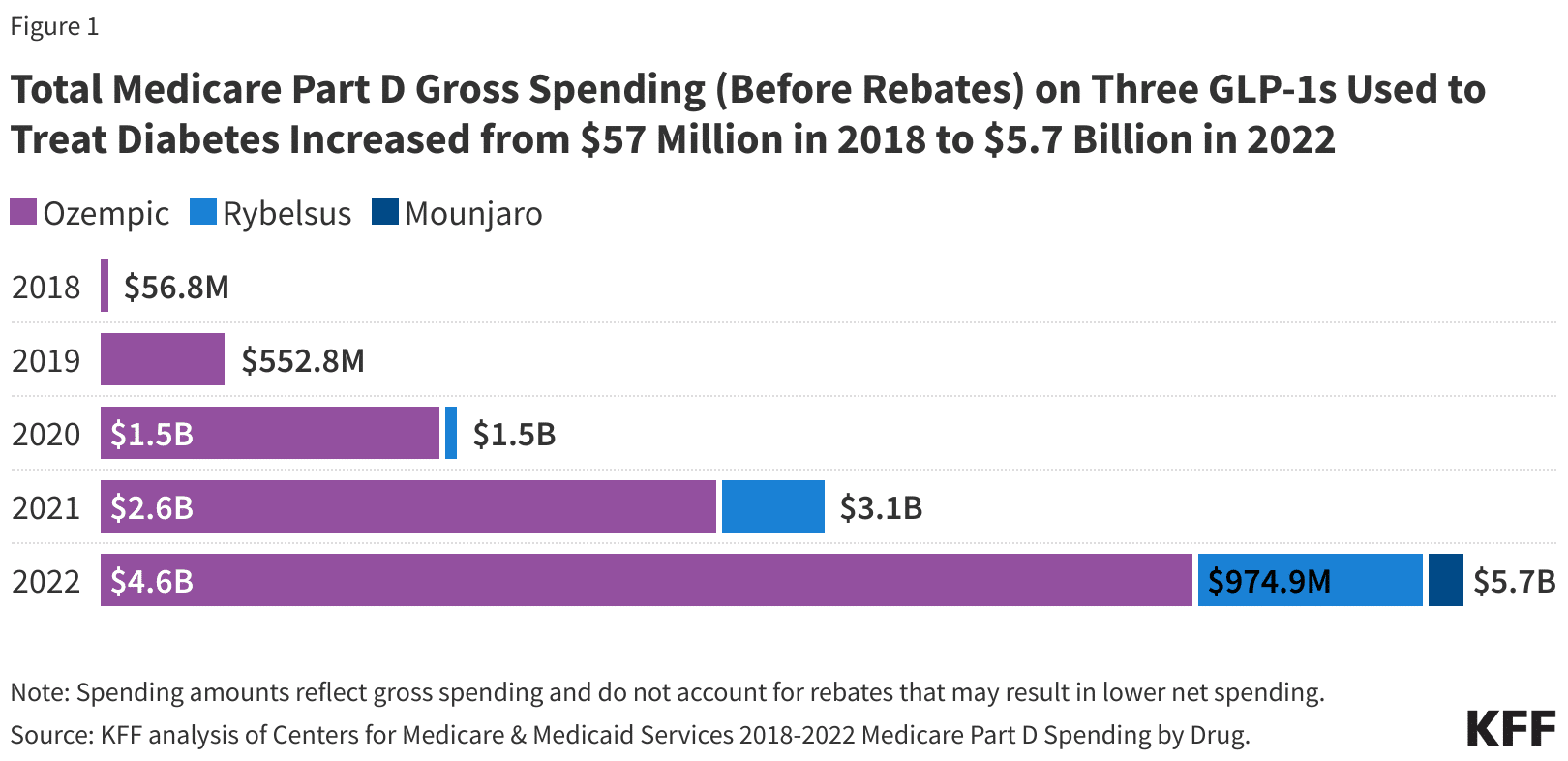

Spending for the three GLP-1 medications, Ozempic, Rybelsus, and Mounjaro, has skyrocketed in the past year on Medicare. While more Medicare beneficiaries are becoming diabetic and using these medications, the number far exceed that type of increase. A significant portion of people on Medicare are now using GLP-1 medications for weight loss.

Medicare Spending on Ozempic Explodes

Impact on Diabetes Patients

The popularity of Ozempic’s off-label use for weight loss is driving a global shortage of diabetes drugs. Pharmacies in the U.S., Canada, and Europe have been reporting shortages. My clients have reported to me their experience of not finding Ozempic at their local pharmacy.

If the shortages persist, people who’ve relied on Ozempic to treat their diabetes may face difficulty adjusting to alternatives. The shortage of Ozempic, driven by its off-label use for weight loss, can have significant consequences for patients with diabetes who genuinely need the medication.

Bottom Line: Medicare Does Not Cover Ozempic for Weight Loss

Ozempic is a dilemma. Most diabetics are overweight, but not all overweight persons are diabetic or pre-diabetic. Medicare does not cover Ozempic for weight loss, but it does cover it for diabetes or pre-diabetes. Weight loss is usually an important element in minimizing the negative effects of diabetes.

While Medicare does not cover Ozempic for weight loss, strictly speaking, Medicare does cover Ozempic for a very large population that also needs and will benefit from Ozempic and losing weight. People aren’t stupid.

It’s actually not a bad solution for an imperfect and overweight world.

Are you feeling lost and confused about Medicare Advantage prior authorization? You’re not alone. Navigating the healthcare system can be overwhelming, especially regarding insurance processes. But fear not—we are here to demystify it all for you.

Are you feeling lost and confused about Medicare Advantage prior authorization? You’re not alone. Navigating the healthcare system can be overwhelming, especially regarding insurance processes. But fear not—we are here to demystify it all for you.

This comprehensive guide will delve into everything you need to know about Medicare Advantage prior authorization. From understanding what it is, why it’s necessary to learn how it works, and the steps involved, we’ll break it down in simple terms. There will be no jargon, no confusing terms—just clear and concise information.

What is Prior Authorization?

Prior authorization is a process used by insurance companies to determine whether they will cover a specific medical procedure, treatment, or prescription drug. It is required for certain services to ensure that they are medically necessary and cost-effective.

Why is Prior Authorization Necessary?

Prior authorization prevents unnecessary medical procedures, reduces healthcare costs, and ensures patients receive appropriate care. Insurance companies can control expenses and ensure that resources are allocated efficiently by reviewing and approving or denying requests for certain healthcare services.

Problems With Medicare Advantage Prior Authorization

However, prior authorization can be complex and time-consuming. It requires healthcare providers to submit detailed information about the patient’s condition, medical history, and proposed treatment plan. The insurance company then reviews this information to determine whether the requested service meets its coverage criteria.

While prior authorization can be beneficial in some cases, it can also lead to delays in care and administrative burdens for both healthcare providers and patients. There are many elements, moving parts, and hands that touch a prior authorization request. Thus, the process is ripe for mistakes, misunderstandings, and delays. Understanding the process and requirements can help you navigate this system more effectively.

Prior Authorization Process for Medicare Advantage

Obtaining prior authorization for Medicare Advantage plans involves several steps. Here’s a breakdown of the process.

Consultation with Healthcare Provider

The first step is to consult with your healthcare provider. They will determine if the service or treatment you need requires prior authorization and initiate the process on your behalf.

Submission of Prior Authorization Request

Once your healthcare provider has determined that prior authorization is necessary, they will submit a request to your insurance company. This request includes all the necessary documentation, such as medical records, test results, and treatment plans. This is where I see problems arise. The doctor’s back office uses incorrect codes, forgets test results, and the doctor’s notes are missing essential language. Then, the request is denied.

Review by the Insurance Company

The insurance company will review the submitted request and evaluate the medical necessity of the service requested. It may also consider factors such as cost-effectiveness and alternative treatment options.

Approval or Denial

Approval or Denial

The insurance company will either approve or deny the prior authorization request based on their evaluation. If approved, you can proceed with the recommended treatment. If denied, you have the option to appeal the decision. The additional problem is the insurance company does not give a reason for the denial, so the provider is clueless about where to begin. The carrier is not required to give a reason, so the provider needs to commit more resources to find out what is needed or let it go.

Appeals Process

You can appeal the decision if your prior authorization request is denied. This involves providing additional documentation or evidence to support the medical necessity of the requested service. The insurance company will review your appeal and make a final determination.

necessity of the requested service. The insurance company will review your appeal and make a final determination.

It’s important to note that the prior authorization process may vary slightly depending on your specific Medicare Advantage plan and the services you need. For detailed information about the process, consult with your healthcare provider, insurance company, and Center for Medicare & Medicaid Services (CMS).

Standard Medicare Procedures & Services Requiring Prior Authorization

Prior authorization is typically required for certain medical procedures, treatments, and prescription drugs. While the specific requirements may vary depending on your Medicare Advantage plan, here are some standard procedures and services that often require prior authorization.

Prior authorization is typically required for certain medical procedures, treatments, and prescription drugs. While the specific requirements may vary depending on your Medicare Advantage plan, here are some standard procedures and services that often require prior authorization.

Specialized Surgeries

Complex surgical procedures, such as organ transplants or bariatric surgery, often require prior authorization. This ensures that the procedure is medically necessary and appropriate for the patient’s condition.

High-Cost Medications

Certain prescription drugs, especially those with high costs, may require prior authorization. This helps insurance companies manage expenses and ensure patients receive appropriate medications.

Imaging Tests

Advanced imaging tests like MRI or CT scans may require prior authorization. This ensures that these tests are necessary and will provide valuable information for diagnosis or treatment.

Physical Therapy or Rehabilitation Services

Medicare Advantage plans often require prior authorization for physical therapy, occupational therapy, or other rehabilitation services. This helps ensure that these services are appropriate and will contribute to the patient’s recovery.

I have found that skilled nursing facility care is very difficult to get approved, especially if the stay exceeds the initial twenty days. The impasse is a combination of the skilled nursing facilities (SNF) refusing to submit for a patient with a Medicare Advantage plan. Many SNFs will not even consider submissions for stays beyond twenty days. Some seem to not know how to properly submit a reauthorization or claim. From the insurance company’s side, their restrictions seem overly prohibitive. This has been a huge source of complaints to CMS and Congress.

Durable Medical Equipment

Durable Medical Equipment

Equipment such as wheelchairs, oxygen tanks, or home healthcare supplies may require prior authorization. This ensures that the items are medically necessary and will improve the patient’s quality of life. CMS has a significant history of fraud, waste, and abuse regarding durable medical equipment.

It’s important to check with your specific Medicare Advantage plan to understand which procedures and services require prior authorization. Your healthcare provider can also provide guidance based on your individual needs.

Benefits of Medicare Advantage Prior Authorization

While the prior authorization process can be perceived as burdensome, it offers some benefits for patients and insurance companies. Here are a few advantages of Medicare Advantage prior authorization:

- Cost control: Prior authorization helps insurance companies control healthcare costs by ensuring that services are medically necessary and cost-effective. This helps keep premiums affordable for all members.

- Appropriate care: Prior authorization ensures that patients receive appropriate care by evaluating the medical necessity of requested services. This helps prevent unnecessary procedures or treatments that may not be beneficial.

- Improved outcomes: By reviewing and approving requests for certain healthcare services, insurance companies can help ensure that patients receive the most effective and evidence-based treatments. This can lead to improved health outcomes and better quality of life.

- Resource allocation: Prior authorization helps allocate healthcare resources efficiently by ensuring that they are used for the most appropriate and effective services. This helps prevent overutilization of healthcare services and ensures that resources are available for those who need them.

While there are benefits to prior authorization, it’s important to acknowledge the challenges and drawbacks of the process as well.

Challenges & Drawbacks of the Medicare Prior Authorization Process

While prior authorization serves a purpose in the healthcare system, it has its challenges and drawbacks. Here are some common challenges that patients and healthcare providers may encounter.

Prior Authorization Administrative Burden

The prior authorization process can be time-consuming and requires healthcare providers to gather and submit extensive documentation. This administrative burden can take away valuable time that could be spent on patient care.

Dr. Jesse M. Ehrenfeld, M.D., president of the AMA (American Medical Association), says,

The need to right-size prior authorization has never been greater—mountains of administrative busywork, hours of phone calls, other clerical tasks that are tied to this onerous review process. It not only robs physicians of face time with patients, but studies show that it contributes to physician dissatisfaction and burnout.

Delayed Care

Prior authorization can sometimes lead to delays in care, as the review process may take time. This can be frustrating for patients who need immediate treatment or services.

Starting in 2026, CMS is shortening the time frames for prior authorization decisions. Insurance payers must respond within 72 hours for an expedited or urgent request and seven calendar days (not business days) for a standard request.

Denial of Coverage

Denial of Coverage

There is always a risk of prior authorization requests being denied. This can be disappointing for patients hoping to receive a particular treatment or procedure.

Lack of Transparency

Insurance companies may have different criteria and guidelines for prior authorization, leading to confusion and lack of transparency. Patients and healthcare providers may struggle to understand the reasons for a denial or how to navigate the process effectively.

Dr. Jesse M. Ehrenfeld, M.D. describes the problem of the lack of transparency with the insurance companies.

When a request is denied, we often don’t know why. We don’t tell you the reasoning behind the denial. It can take hours and hours to appeal a decision. And then sometimes you wait weeks or even months for a peer-to-peer consult.

The CMS final rule will require insurers to provide specific, very specific denial reasons and public reporting of metrics. How often do they approve? How often do they deny things? How long does it take for a process to actually give a result for a request?

Insurers will also be required to share that information with patients, so that our patients can become informed decision makers when they buy health insurance on the exchanges and make planned decisions. That’s going to begin in 2026 and will go a long way in bringing much-needed transparency and accountability to the entire process.

Appeals Process

While the option to appeal a prior authorization denial exists, it can be a lengthy and complex process. Patients may need to provide additional documentation and evidence to support their case, which can be challenging and time-consuming.

In the efforts to improve the Medicare Advantage prior authorization process, CMS will require, according to Dr. Ehrenfeld,

Plans to support an electronic prior authorization process that’s embedded in the physician’s electronic health records, bringing much needed automation and efficiency to our current very manual and very time-consuming workflow. That change is going into effect in 2027—it’s going to be a game-changer for everybody.

So having direct integration of prior authorization into the EHR (electronic health record) is going to significantly reduce the burden on physicians. And this is where so much of that $10 to $15 billion in savings is going to come from.

Despite these challenges, some strategies and tips can help you navigate the prior authorization process more effectively.

Navigating the Prior Authorization Process Effectively

Navigating the Prior Authorization Process Effectively

Navigating the prior authorization process can be overwhelming, but with the right strategies, you can streamline the process and ensure a smoother experience. Here are some tips to help you navigate prior authorization effectively:

Understand your Medicare Advantage Plan

Familiarize yourself with your Medicare Advantage plan’s specific requirements and guidelines. This will help you understand which procedures and services require prior authorization and what documentation is needed. This is important because you may have to be the force behind the doctor’s office to pursue approval beyond the initial request.

Communicate with Your Healthcare Provider

It is crucial to communicate openly and clearly with your healthcare provider. They can guide you through the prior authorization process, provide necessary documentation, and advocate for your needs. The office needs to see that you want the procedure or test because they have limited resources to pursue further requests or appeals from the insurance company.

Gather All Necessary Documentation

Before submitting a prior authorization request, ensure you have all the necessary documentation. This may include medical records, test results, treatment plans, and any additional information requested by your insurance company. If you can assist in the process, then dig in. You may also have to be the supervising authority to make sure the office’s back office submits all relevant materials.

Be Proactive

Start the prior authorization process as early as possible to avoid delays in care. Submit your request well in advance of your scheduled procedure or treatment to allow ample time for review. Doctor’s offices are usually overworked and understaffed. To ensure you are taken care of in a timely way, contact the office yourself to see where your prior authorization is in the process. Ask for dates when you should expect tasks to be completed by the doctor’s office and insurance company.

Keep Copies of All Documents

Make copies of all documents related to the prior authorization process, including your request, supporting documentation, and any communication with your insurance company. This will help you stay organized and provide evidence if needed for an appeal. The documents are your records. You and the insurance company paid for the tests, and you have a right to your own copies.

Follow Up with Your Insurance Company

Stay proactive and follow up with your insurance company to ensure your prior authorization request is processed. This will help you stay informed and address any issues or concerns in a timely manner. Everyone is busy. Balls are dropped. People forget. You make sure none of that happens with your case because you are on it.

How to Appeal a Prior Authorization Denial

If your prior authorization request is denied, you have the option to appeal the decision. Here’s a step-by-step guide on how to appeal a prior authorization denial.

- Understand the denial: Carefully review your insurance company’s denial letter. Understand the reasons for the denial and the specific requirements for appealing the decision.

- Gather additional documentation: If you believe that the denial was made in error or that additional information could support your case, gather all the necessary documentation. This may include medical records, test results, or a letter of medical necessity from your healthcare provider. Your provider will need to perform most of this work.

- Submit an appeal letter: Write a formal appeal letter to your insurance company. Generally the doctor will need to draft and submit the letter. He will need to more clearly state the reasons for your request, provide supporting documentation, and explain why you believe the requested service is medically necessary.

- Follow up with your insurance company: This is where you can help the process. Stay in contact with your insurance company to ensure your appeal is processed. Follow up regularly. You will be able to follow up more readily than the provider’s office. Get any additional information or documentation requested.

Remember, the appeals process may take time, and no approval is guaranteed. However, following these steps and providing compelling evidence increases your chances of a favorable outcome.

Bottom Line: Understanding Medicare Advantage Prior Authorization May Determine Your Success

In conclusion, understanding and managing Medicare Advantage prior authorization is crucial for both patients and healthcare providers. While the process can be complex and time-consuming, it ensures that healthcare services are medically necessary and cost-effective.

By familiarizing yourself with the prior authorization process, understanding your Medicare Advantage plan requirements, and effectively communicating with

your healthcare provider and insurance company, you can navigate this system with confidence and ease.

Remember to stay proactive, gather all necessary documentation, and be prepared to advocate for your needs. In the event of a denial, don’t hesitate to appeal and seek assistance if needed.

Empower yourself with knowledge and take control of your healthcare journey. With the right information and resources, you can successfully navigate Medicare Advantage prior authorization and receive the care you need.

Are you in the lucky top 4% of earners? You will pay more for your Medicare benefits. The more is IRMAA (Income-Related Monthly Adjustment Amount). The amount you pay for your Medicare health and prescription drug coverage depends on your level of income. There is a ladder.

Are you in the lucky top 4% of earners? You will pay more for your Medicare benefits. The more is IRMAA (Income-Related Monthly Adjustment Amount). The amount you pay for your Medicare health and prescription drug coverage depends on your level of income. There is a ladder.

Would you like to avoid paying that tax or possibly pay a smaller portion of it? We will guide you through the key IRS exceptions for Medicare IRMAA (Income-Related Monthly Adjustment Amount). By understanding and leveraging these exceptions, you can potentially lower your Medicare expenses and put more money back in your pocket.

Medicare IRMAA is an additional premium that high-income Medicare beneficiaries are required to pay. However, there are exceptions that may enable you to reduce or even eliminate this extra cost. Knowing the ins and outs of these exceptions can make a significant difference in your healthcare expenses.

In our comprehensive guide, we will break down each exception and provide you with the information you need to take advantage of them. From ‘Life-Changing Events’ to ‘Reconsideration Requests,’ we will explore all the options available to you.

Understanding the IRS Exceptions for IRMAA

The Income-Related Monthly Adjustment Amount, or IRMAA, is an additional premium that high-income Medicare beneficiaries have to pay. However, the IRS provides exceptions that may allow you to reduce or eliminate this extra cost. Let’s explore these exceptions in detail.

Life-Changing Event

Life-Changing Event

One of the exceptions to IRMAA is a life-changing event. This includes events like marriage, divorce, death of a spouse, or work stoppage. If you experience any of these events, you may be eligible for a reduction in your Medicare costs.

To qualify for this exception, you will need to provide documentation of the life-changing event and submit it to the IRS. Documentation is key. The IRS will not take your word for it. You need to prove your income decreased.

Examples of documentation may include a marriage license or divorce decree, death certificate, or proof of work stoppage. By leveraging this exception, you can potentially save a significant amount of money on your monthly Medicare premium.

Medicare IRMAA Exception 1: Marriage or Divorce

Getting married or divorced can have a significant impact on your income and, consequently, your Medicare costs.

If you are recently divorced and you are a lower income earner, you may drop below the IRMAA threshold or at least step down the ladder, which would reduce your tax.

For some individuals, marriage may reduce their income because alimony is lost. The threshold is increased because it is for two persons. The initial threshold for a single individual is $103,000. For married filing jointly, it is $206,000. Either of these lifestyle changes may affect your income in that year and, consequently, your IRMAA tax, even if your income was higher in the previous year.

To take advantage of this exception, you must provide documentation of the marriage or divorce and proof of the change in income. By doing so, you can potentially save a significant amount on your Medicare expenses.

Medicare IRMAA Exception 2: Work Stoppage or Reduction

If you experience a work stoppage or a significant reduction in your work hours, you may be eligible for an exception to IRMAA. This can happen if you retire, get laid off, or experience a reduction in your income due to other circumstances. This is probably the most common reason high-income earners should apply for the exception. Their income was significantly higher the previous year because of work, but the year they retire and must pay the Medicare premium, their income is drastically smaller. That is what the exception is for.

To qualify for this exception, you will need to provide documentation of the work stoppage or reduction in work hours, along with proof of the decrease in income. By doing so, you can potentially reduce or eliminate the additional premium you have to pay.

Medicare IRMAA Exception 3: Loss of Income-Producing Property

If you experienced a loss of income-producing property, such as rental properties or investments, you may be eligible for an exception to IRMAA. This can happen if your rental property becomes unprofitable or if you experience significant losses in your investments.

I had a high-net-worth client who lost significant rental income because of flooding in Missouri. His properties produced nothing for several years as he settled with insurance companies and repaired buildings.

I had a high-net-worth client who lost significant rental income because of flooding in Missouri. His properties produced nothing for several years as he settled with insurance companies and repaired buildings.

To qualify for this exception, you will need to provide documentation of the loss of income-producing property, along with proof of the decrease in income. By leveraging this exception, you can potentially lower your Medicare costs and save money.

Medicare IRMAA Exception 5: Loss of Pension Income

Pension plans go bankrupt. Some pensions are for a particular duration. The cessation of a pension may impact your income significantly enough to affect the IRMAA tax.

To qualify for this exception, you will need to provide documentation of the change in income, along with proof of the decrease in income. By taking advantage of this exception, you can potentially reduce or eliminate the additional premium you have to pay.

Medicare IRMAA Exception 6: Employer Settlement Payment

Employers pay out settlements to employees for many reasons. These settlements may increase income in a given year or for several. The settlement may have its own legal stipulations.

To qualify for this exception, you will need to provide documentation of the change in income, along with proof of the decrease in income. Some legal settlements may be placed legally outside of your modified adjusted gross income. By taking advantage of this exception, you can potentially reduce or eliminate the additional premium you have to pay.

Medicare IRMAA Exception 7: Correcting An Erroneous Determination

Sometimes, the IRS may make an erroneous determination regarding your Medicare costs. If you believe that the IRS made a mistake in calculating your IRMAA, you can submit a reconsideration request and provide additional documentation to correct the error.

To qualify for this exception, you will need to provide evidence that the IRS made an error in its determination. This can include documentation of your income, tax returns, or any other relevant information that supports your case. Correcting an erroneous determination can potentially save you a significant amount on your Medicare expenses.

Applying for a IRMAA exception

To apply for an exception to IRMAA and reduce your Medicare costs, you will need to follow a few steps.

First, gather all the necessary documentation to support your case. This includes marriage or divorce certificates, death certificates, proof of work stoppage or reduction, documentation of the loss of income-producing property, proof of a change in tax-exempt income, or evidence of an erroneous determination.

Next, complete the appropriate forms provided by the IRS SSA-44 (12-2023). These forms may vary depending on the exception you are applying for. Make sure to fill them out accurately and include all the required information.

Once you have completed the forms, submit them to the IRS along with the supporting documentation. It is crucial to keep copies of all the documents and forms for your records.

After submitting your application, the IRS will review your case and make a determination. If your exception is approved, you will receive a notification informing you of the reduction or elimination of your IRMAA.

By applying for an exception and reducing your Medicare costs, you can put more money back in your pocket and have a significant impact on your overall healthcare expenses.

Bottom Line: Don’t Ignore the IRMAA Exceptions

Leveraging the key IRS exceptions for IRMAA can reduce your Medicare costs. Whether you have experienced a life-changing event, a change in income, or an erroneous determination, understanding these

Christopher J. Grimmond

exceptions can significantly reduce your healthcare expenses.

Don’t let high-income Medicare premiums burden your finances. Take the necessary steps to apply for an exception and potentially reduce or eliminate your IRMAA. By doing so, you can save money and have more control over your healthcare expenses.

With the rising prevalence of cancer diagnoses, obtaining affordable and accessible cancer drug coverage with Medicare is critical for patients. Medicare, the government health insurance program primarily for individuals age 65 and older, is vital in ensuring that cancer treatments are financially attainable. Many of my clients will call me when they receive a diagnosis of cancer. As you can imagine, the experience is overwhelming and frightening. Their first question is what they should do about their insurance to ensure maximum coverage.

With the rising prevalence of cancer diagnoses, obtaining affordable and accessible cancer drug coverage with Medicare is critical for patients. Medicare, the government health insurance program primarily for individuals age 65 and older, is vital in ensuring that cancer treatments are financially attainable. Many of my clients will call me when they receive a diagnosis of cancer. As you can imagine, the experience is overwhelming and frightening. Their first question is what they should do about their insurance to ensure maximum coverage.

This article will explore the implications of Medicare’s cancer drug coverage on affordability and access. We will consider the various components of Medicare, including Part B and Part D, and how they differ in covering cancer drugs. Additionally, we will examine the potential out-of-pocket costs that Medicare beneficiaries may face and discuss strategies to navigate these expenses.

Aspects such as drug tiers, formularies, and specific cancer treatments covered by Medicare will also be explored. By the end of this article, you will understand the implications of Medicare’s cancer drug coverage on affordability and access. You will be empowered to make informed decisions regarding your healthcare needs.

Understanding the Implications of Medicare Coverage for Cancer Drugs

Medicare provides crucial coverage for cancer drugs, ensuring beneficiaries can access potentially life-saving treatments. However, it’s important to understand the implications and costs of this coverage to make informed decisions and navigate the system effectively.

Part B Or Part D

One key aspect to consider is the difference between Medicare Part B and Part D coverage for cancer drugs. Medicare Part B covers drugs administered in a medical setting, such as chemotherapy drugs. These drugs are typically covered at 80% of the Medicare-approved amount, with the remaining 20% being the beneficiary’s responsibility. Part B coverage is often more comprehensive for cancer treatments, including essential drugs like intravenous chemotherapy and supportive medications.

When clients tell me their medication falls under Part B, I am relieved. Treatments, like chemotherapy drugs, insulin pumps, and Prolia injections in the doctor’s office, are completely covered when you have Original Medicare and a Medicare Supplement. On Medicare Advantage, there is a maximum out-of-pocket that puts at least a cap on costs.

Part D Formularies

On the other hand, some oral cancer medications and medications used for supportive care, such as anti-nausea drugs, are placed under Part D prescription drug plans. Private insurance companies approved by Medicare offer Part D plans, and coverage may vary depending on the specific plan. Medicare Part D prescription drug plans are not as robust in their coverage compared to Part B.

prescription drug plans. Private insurance companies approved by Medicare offer Part D plans, and coverage may vary depending on the specific plan. Medicare Part D prescription drug plans are not as robust in their coverage compared to Part B.

It’s important to carefully review Part D formularies, which are lists of covered drugs, to ensure that the necessary cancer medications are included. Expensive medications, including expensive cancer drugs, are very expensive on a Medicare Part D plan. While there are limitations, and in 2025 there will be a $2,000 cap, generally, the medications are still very expensive if they are covered.

Understanding the differences between Part B and Part D coverage is crucial for effectively navigating Medicare’s cancer drug coverage. You may not have much choice when it comes to cancer drug treatment and where it falls in terms of Medicare insurance. But, by knowing which drugs fall under each part, beneficiaries can determine the most appropriate coverage for their specific needs and minimize out-of-pocket costs.

Accessing Affordable Cancer Drug Coverage Under Medicare

Accessing Affordable Cancer Drug Coverage Under Medicare

While Medicare plays a significant role in providing cancer drug coverage, beneficiaries may face challenges and barriers when trying to access affordable medications. These issues can impact both the affordability and availability of cancer drugs, making it difficult for patients to receive the treatments they need.

High Cost

One common challenge is the high cost of cancer drugs. Many cancer medications come with a hefty price tag, and even with Medicare coverage, beneficiaries may still face substantial out-of-pocket costs. This can create financial burdens, especially for those with fixed incomes or limited financial resources. Additionally, certain cancer drugs may not be covered by Medicare, leaving beneficiaries to shoulder the entire cost themselves.

Confusing System